Nobody wants to deal with debt collectors. Unfortunately, you may have no choice but to deal with them – even if you don’t owe them anything.

If that sounds absurd, that’s because it is.

More than half (53%) of complaints in the CFPB’s latest annual “Fair Debt Collection Practices Act” report[1] are “attempts to collect debt not owed.” The report shows that 6,500 Americans allege debt collectors “threatened to take negative or legal action.”

You have rights. Below we explain everything you need to know about debt collections: How it works and what can and can’t be held against you legally.

Table of Contents

Understanding the collection process

Missing a few payments shouldn’t spell the downfall of your financial health. Yet, that concern can turn to panic once a debt collector begins to call. The reality is that the calls typically won’t begin until you miss six payments. That gives you quite a bit of time to address the past-due account before it gets sent to a collector.

If you can’t rectify the situation, however, it will go to collections. Here’s everything you need to know about the debt collection process:

Phase 1: The creditor moves the delinquent account to a “charge-off” status

This means that the creditor effectively writes off your account as a loss. The account gets frozen, and you can’t make purchases with it.

Phase 2: The creditor sends the debt to a collector

Collectors are the ones that come after you. Debt collectors are people, agencies, or companies whose responsibility is to collect owed money. They can be an in-house collection department or a third party.

In some cases, the original creditor will keep the account and simply let collectors work on their behalf. In other situations, they will sell the debt to an independent third-party collector. That changes who you owe and has other implications we go into more detail below.

Phase 3: Contact governed by the FDCPA

After a debt goes to a collector, they will try and get in touch with you to confirm they have the correct contact information and correct holder of said debt. Any conversations they have with you must adhere to a 46-year-old law called the Fair Debt Collection Practices Act, which was “designed to eliminate abusive, deceptive, and unfair debt collection practices.”

Phase 4: Identity confirmation

Once the collector verifies the holder of the debt, you will get a written “validation notice” which arrives within five days. It will state who the original creditor is, who owns the debt now, how much you owe and how to move forward.

If you do not receive this letter, request it and do not agree to any conversations about the debt until you receive it.

Phase 5: Facing collections head-on

The instructions for how to proceed will be on your validation notice, you have a few options you can take.

If you owe the debt and have the means, paying is the easiest way to make the collector go away. Be aware that paying in full may not remove the collection account from your credit report or immediately improve your credit score. A debt settlement plan may be a better option. This allows you to negotiate with the collector to pay back less than what you owe. If you’d like more information, give us a call at .

If you don’t believe you owe the debt or believe the collector doesn’t have the legal right to collect, you can dispute the debt. The collector must send additional verification that you owe the debt, and they have a legal right to collect.

You can also simply tell the collector you do not want them to contact you. You simply write a cease-and-desist letter, and they must stop all content. However, they can sue you and take you to court.

Collectors only have a limited time to take you to court. The statute of limitations for debt collection varies from state to state, but it’s a maximum of 15 years. Many states limit it to 6. So, you can wait it out, dodge those collection calls and then once the statute expires, then send a cease and desist.

Always verify a collection account

Debt validation is a legally granted right under the FDPCA. The law mandates that within five days of the collector’s first contact, they must send you a written letter validating the debt.

This notice MUST include how much debt is due and the name of the creditor that owns the debt. If you do not respond within 30 days to dispute the debt, it becomes valid.

It is important that before you make any agreements to pay back the debt you make sure the debt is correct and valid. When debt buyers “buy” your debt, the full information isn’t always given to them. If collectors don’t have the required information, they have no legal right to collect.

Debt collection as a small business owner

As a small business owner making money and growing is your number one priority. But when people don’t pay the money they owe, it can be tough to survive. For growing businesses, unpaid invoices can cripple the finances of the business and even the owner. In this case, you become the collector or need to hire one on your behalf.

While putting on your collector hat can be frustrating, it’s important to understand the impact that collections can have on your business. Why businesses need to take them seriously.

Dealing with debt collections when you are on the hook

Having debt can take a toll on many aspects of your life and if you’ve resolved to become debt-free, debt settlement is one way to do it. Debt settlement is typically the fastest way to get out of credit card debt outside of Chapter 7 bankruptcy, and it usually works best for debts in collections.

It works in three basic ways:

- Respond to a settlement offer sent by a collector

- Try negotiating on your own

- Contact a settlement company or get a referral to an accredited company through Debt.com

A word of advice, debt settlement works differently, depending on the type of debt you need to settle. So, if you’re unsure what type of settlement program you need, call

Deciding to settle your debt is a big decision. It can help you get out of debt for less than you owe, but you must weigh the consequences of credit damage you’ll likely face. On average, the settlement of one credit card would drag your score down by 45-65 points if your FICO score was 680. The higher your score, the more points you drop.

Facing a collection lawsuit

A collection lawsuit occurs when you default on an unsecured loan or fail to pay a credit card off before it gets moved to charge-off status. When a company exhausts its resources trying to get you to pay the debt it will either sue you for payment or sell the debt to another company. Take note, that while you can get sued by either company, it must be before the statute of limitations expires.

The time this takes differs from state to state, so it’s important to look at how old the debt is. The most important thing to know when facing a civil summons for a lawsuit is to NEVER ignore it. It will not protect you from the consequences you would face in court and a judgment can get filed against you even if you’re not there.

Dealing with debt collections you don’t owe

The first thing to do when you get a call concerning a debt is to verify it.

Get the name of the collector and their company, as well as all other pertinent information, such as the original creditor you owed. Fake debt collectors are a real thing, so make sure to be on the lookout. If you don’t recognize the debt, if they refuse to give you their phone number or address or they try to scare you into paying, it should be an immediate red flag.

If you are still burdened by calls, a cease-and-desist letter can be one way to get the harassment to stop. Federal law requires that collectors cannot contact you once you send one, but they can still sue you. Should you find yourself in a situation where a collector hounds you for a debt you do not owe, a cease-and-desist letter is the way to go. If they take you to court, you must demonstrate you don’t owe the debt and the case should be settled in your favor.

Click here to get free cease-and-desist templates from Debt.com »

If you know that you’ve been on the hook for debt in the past, make sure you look into the statute of limitations in your state. This is the legal amount of time that a collector can sue you for a debt. Should the specified amount of time pass, the debt is still there but legal action cannot arise. The collector can contact you but if you send a cease and desist, then even that contact must stop.

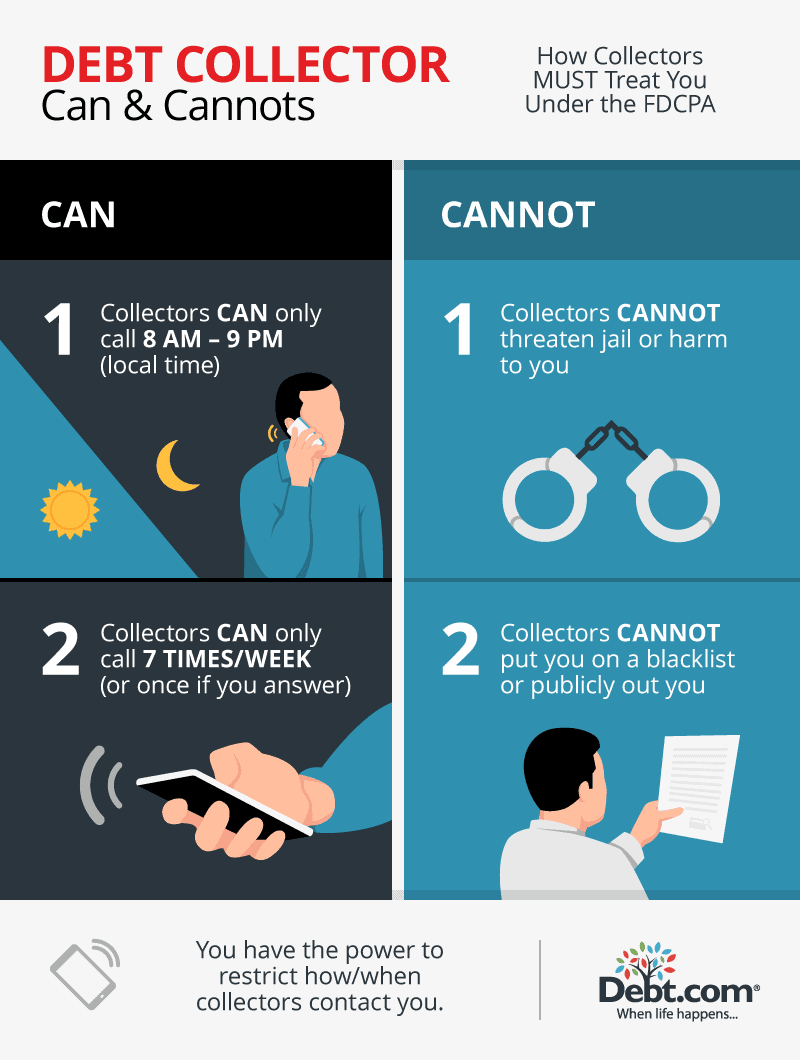

How the FDCPA protects against collector abuse

The FDCPA keeps you protected against unlawful collection tactics. Collectors can be aggressive when attempting to collect a debt, but they can only go so far within the boundaries of the law. Put into practice in 1978 as part of the Consumer Credit Protection Act,[2] the FDCPA establishes standards for debt collectors.

In most cases, the Federal Trade Commission (FTC) enforces these rules. A very important thing to remember is even if you legitimately owe a debt, you still have rights. The FDCPA is there to protect you, don’t be afraid to report harassment.

The following graphic provides a breakdown of the most essential regulations of the FDCPA:

How to make a complaint against a collector

If you’ve been the victim of harassment from a debt collector, there are steps you can take depending on your goal. From suing the debt collector to reporting them to government agencies, to even using the violations as a negotiation tactic. And though you may not think of it as harassing, around 40% of complaints stem from repeated or continuous calling practices.

Check on the guidelines in the FDCPA and make sure that what happened to you violated the law. Keep in mind that if you are just filing a complaint, that is not enough to grant you any money. If you want compensation in the form of a harassment lawsuit, Debt.com can connect you to professionals to help you do this. If you need help with an abusive collector, give us a call at or complete the form below. Once we’ve connected you with the right resources to stop the harassment, we can connect you with the right experts to take care of your debt as well.

Find solutions to pay off debt and get on the right financial track.

Suing a debt collector for harassment

The FDCPA outlines how collectors can communicate with you and what practices are adherently prohibited. Once a collector violates the law, you have the right to file a complaint and sue them in civil court. In 2023, the latest available data, there were 109,900 complaints filed with the CFPB.[1]

Should you win your lawsuit, you can get two types of damage litigations:

- Actual damages, which is any money you’ve lost because of abuse or threats.

- Statutory damages, which offer extra compensation up to $1,000 total, based on the level of abuse or number of violations.

Collectors cannot harass you. This means that they can’t:

- Use threats of violence

- Use profanities

- Continuously call you

Lying is a backhanded tactic they will use if they believe you do not know the law. This can entail:

- Telling you a higher amount than you owe

- Threaten you with legal action or arrest

- Impersonating an attorney

Take heed and learn all the ways to protect yourself from shady collectors.

Debt collections and your credit

People believe that if you pay off a debt in collections it removes the damaging mark from your credit. The debt will appear on your credit report as paid, but it will remain on there for the next seven years in most states.

Collections can have a significant impact on your credit score. The damage will lessen over time, but when it is initially reported, you will see the steepest drop.

The impact of debt collections on your score depends on a range of factors. Your FICO credit score when a debt goes to collections and if the account gets sold to a third party are two of the more important factors taken into account. For example, collections affect your score more if your score was high before the collection account happened. If the debt gets sold to a third party, the collector can report a separate collection account in your credit report.

If you are struggling with collectors or your credit score, Debt.com is here for you. Give us a free call at and see what your options are.

Debt Collection FAQ

No. Under the Fair Debt Collection Practices Act (FDCPA), it prohibits collectors from calling family, friends, or neighbors to collect on a debt or report that you owe them. However, collectors can call anyone they see fit to verify your identity. Once your identity and contact information gets verified, the call must end. If the call does not end there, or the collector discloses anything about how much is due, who is collecting, or how long the debt has been past due, you can file a collector harassment complaint.

Find out more about who debt collectors can call and what they can disclose »

No. Collectors are not allowed to call your place of employment in regard to any bills you may owe them. Third-party debt collectors are bound by the Fair Debt Collection Practices Act. Creditors are free to reach out to verify employment or request your address or phone number. But they can only verify your identity.

The only people that debt collectors may reach out to, to discuss anything related to your debt are you, your spouse, or an attorney. No bosses, clients, coworkers, friends, distant relatives, etc. If a debt collector tries harassing other people to goad you into paying, you have a case for a harassment suit.

Learn more about who debt collectors can legally call »

In simple terms, no. Creditors do not have the authority to seize your money or force you into selling your assets. They can however sue you and take you to court in an effort to collect the debt. But the law doesn’t necessarily stop collectors from making threats. This is especially common with seniors, even though things like Social Security income are often protected.

Eric Olsen, executive director of HELPS nonprofit law firm advises, “There are many reasons why a senior doesn’t need to fear a judgment lien. Seniors often don’t realize the federal and state laws that protect their money from debt collectors. And because of this protection, many credit card companies see that it’s not economical to sue seniors for past-due debt in the first place.”

Understand more about how your assets stay secure here »

According to the law, collection agencies have the right to deny any partial payments as they see fit. They are also not obligated to work with you on any payment schedules or reductions. The goal of these agencies is to collect back the money owed as quickly as possible. Take note that in the major types of debt (credit cards, utilities, medical debt and mortgages) you do have different terms and policies which could affect your payments.

Learn more about the differences in each type of debt »

There is a 3-step process when you get sued by a creditor. First, make sure not to ignore it. Respond to the summons for the lawsuit by the date specified, as it forces the collector to prove you owe what you owe. This will be the time to request a debt verification letter.

Second, consider an attorney who specializes in debt. If you can afford professional guidance, it can help you in responding to the lawsuit and in some cases, work out a deal to drop the lawsuit. You can also find free legal aid in your area.

Lastly, bankruptcy should be an option. While it shouldn’t be your first resort, it can be a viable last resort. If you are overwhelmed with debts and collection accounts, it’s the easiest way to discharge all of them at once.

Find more information on what your course of action should be when you’re sued by a creditor »

In accordance with the Fair Credit Reporting Act, or FCRA, most negative items on your credit report must get removed after seven years. While this does get you off the hook in terms of your credit, you may still technically be on the hook for the debt. The debt doesn’t just disappear. Each state has its own statute of limitations, where agencies have as few as three years and as many as fifteen years to take you to court.

Understand the full scope of creditors and what your options are »