Debt.com’s writers are journalists, personal finance experts, and certified credit counselors. Their advice about money – how to make it, how to save it, and how to spend it – is based on, collectively, a century of personal finance experience. They’ve been featured in media outlets ranging from The New York Times to USA Today, from Forbes to FOX News, and from MSN to CBS.

Debt.com and Florida Atlantic University Survey: Credit Card Debt Didn’t Soar During Pandemic

As the pandemic winds down, new research shows credit card debt didn’t reach record highs in the U.S. as finance experts originally predicted. But it turns out the most likely to survive COVID-19 were least immune to credit card debt.

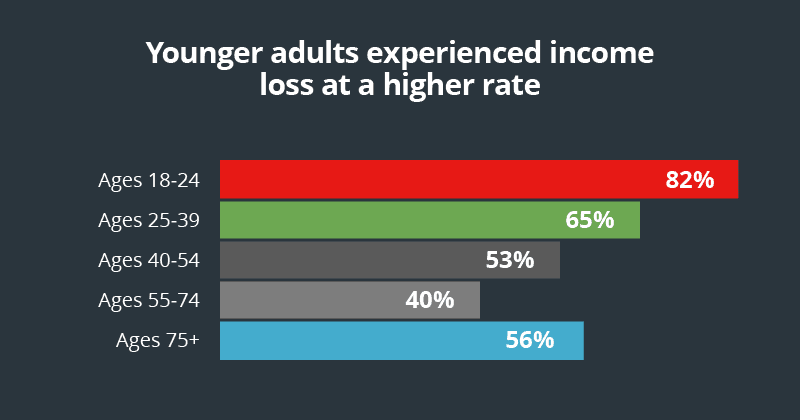

Those who suffered most were the youngest.

As the pandemic winds down, new research shows credit card debt didn’t reach record highs in the U.S. as finance experts originally predicted. But it turns out the most likely to survive COVID-19 were least immune to credit card debt.

By last July, more than 50 million Americans found themselves out of work due to government-ordered shutdowns. Today, a nationwide survey reveals most of them were in the early phase of their careers and had no choice but to take on credit card debt to make ends meet.

The survey of 1,000 Americans conducted by Florida Atlantic University’s Business and Economics Polling Initiative (FAU BEPI) – a polling institute that conducts surveys on business, economics, political and social issues to gauge attitudes and opinions at regional state and national levels – shows the majority of Americans made it through the pandemic without charging up large credit card bills. That’s with the exception of everyone under 39 years old. They got nailed.

Roughly 3 in 5 Millennials (ages 25-39) replied yes when asked, “Did the COVID-19 pandemic cause any income loss in your household?” That number shot up to 82 percent when members of Generation Z (ages 18-24) answered yes to that question. It seems the income loss led to credit card usage to survive.

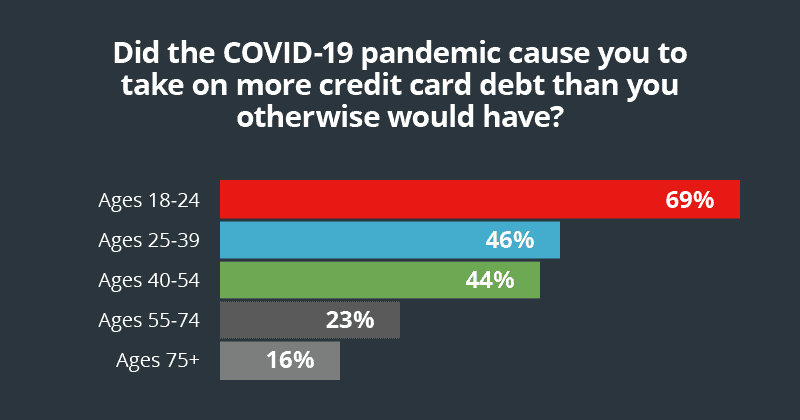

Nearly 70 percent of Gen Z respondents said the pandemic, “caused them to take on more credit card debt than they otherwise would have.” That number dropped for Millennials, but not much: 46 percent answered yes when asked.

Nearly 6 in 10 of Gen Z respondents had to stop making payments on their credit cards. The same for 4 in 10 of Millennials who took the survey.

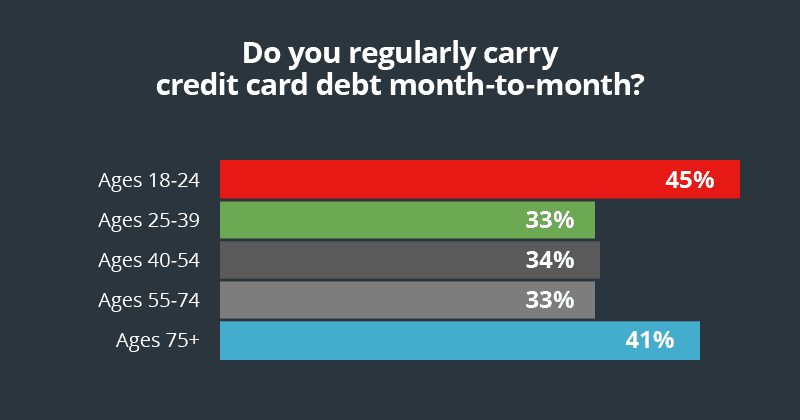

The data shows the finances of Gen Zers and Millennials were already fragile. More than 4 in 10 respondents ages 18 to 24 said, “they regularly carry a credit card balance month-to-month.”

“It’s devastating to hear the career path of our nation’s future began with a patch of thin ice. So many have already fallen into a dangerous place,” said Don Silvestri, president of Debt.com. “Millennials carry so much baggage leftover from the last economic downturn. It’s a shame to see the next generation now facing a similar dilemma. One can only hope as the economy recovers, our young workforce can find a lifeline and get back on stable ground.”

For more information on how younger workers took on more credit card debt during the pandemic, read the full Americans’ Views on Their Personal Finances Before and After COVID-19 Report and infographic focused on Millennials and Generation Z findings.

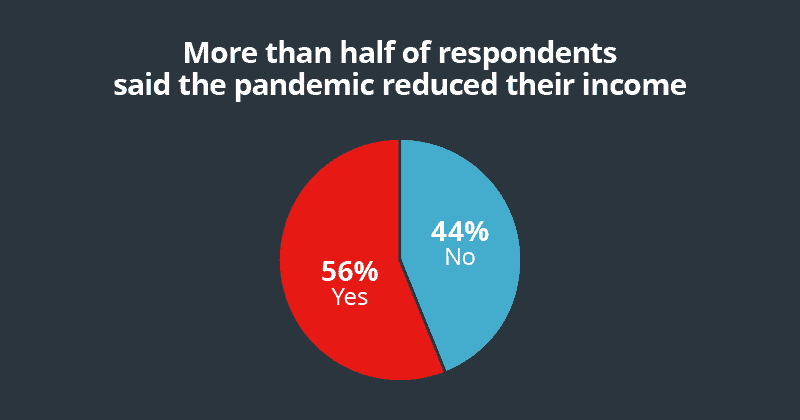

The pandemic caused most respondents to lose income

Generation Z and Millennials reported higher rates of income loss due to the pandemic

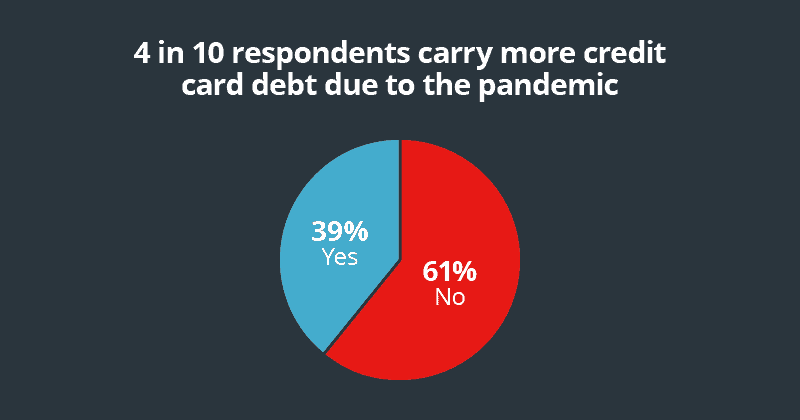

Most respondents say the pandemic didn’t cause them to take on more credit card debt

More Gen Z and Millennial respondents reported taking on credit card debt due to the pandemic

Not surprising, younger respondents always carry some kind of credit card debt month-to-month

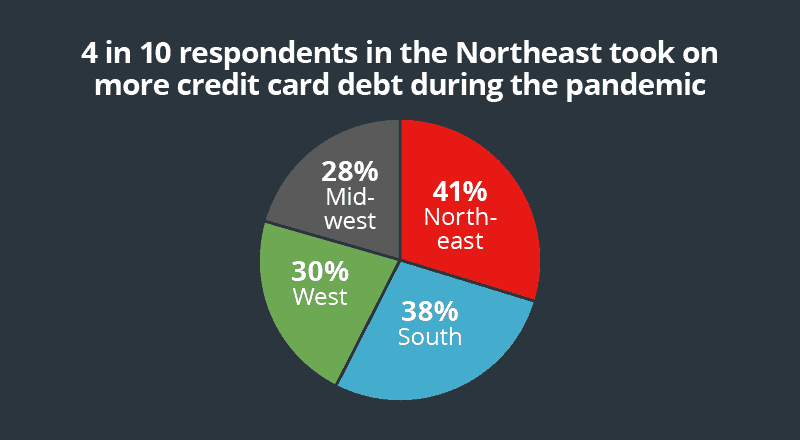

Respondents living in the Northeast took on credit card debt more than the rest of the country

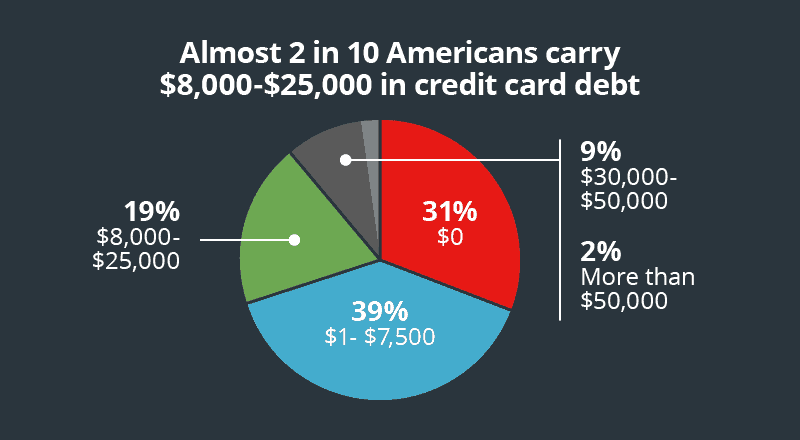

Most survey respondents said they carry up to $7,500 in credit card debt

For full survey results, click here

Did the COVID-19 pandemic cause any income loss in your household?

Yes

No

Percentage of respondents

55.8%

44.2%

Did the COVID-19 pandemic cause any income loss in your household? By generation

Yes

No

Ages 18-24

81.8%

18.2%

Ages 25-39

64.5%

35.5%

Ages 40-54

53.1%

46.9%

Ages 55-74

39.5%

60.5%

Ages 75+

55.6%

44.4%

Did the COVID-19 pandemic cause any income loss in your household? By Region

Yes

No

Northeast

61.7%

38.3%

Midwest

40.4%

59.6%

South

53.2%

46.8%

West

70.0%

30.0%

Did the COVID-19 pandemic cause you to take on more credit card debt that you otherwise have?

Yes

No

Percentage of respondents

39.1%

60.9%

Did the COVID-19 pandemic cause you to take on more credit card debt that you otherwise have? By Generation

Yes

No

Ages 18-24

69.2%

30.8%

Ages 25-39

46.2%

53.8%

Ages 40-54

44.4%

55.6%

Ages 55-74

23.3%

76.7%

Ages 75+

15.6%

84.4%

Did the COVID-19 pandemic cause you to take on more credit card debt than you otherwise would have? By Region

Yes

No

Northeast

51.3%

48.7%

Midwest

28.4%

71.6%

South

37.0%

63.0%

West

42.4%

57.6%

How much credit card debt do you currently owe?

Percentage of respondents

$0

31.2%

$1 to $7,500

38.8%

$8,000 to $25,000

18.9%

$30,000 to $50,000

8.8%

More than $50,000

2.3%

How much credit card debt do you currently owe? By Generation

$0

$1 to $7,500

$8,000 to $25,000

$30,000 to $50,000

More than $50,000

Ages 18-24

23.3%

34.2%

26.7%

11.7%

4.2%

Ages 25-39

27.2%

38.2%

23.2%

9.6%

1.8%

Ages 40-54

26.2%

52.5%

16.0%

4.9%

0.4%

Ages 55-74

37.8%

39.5%

17.3%

2.7%

2.7%

Ages 75+

44.4%

8.9%

8.9%

33.3%

4.4%

How much credit card debt do you currently owe? By Region

$0

$1 to $7,500

$8,000 to $25,000

$30,000 to $50,000

More than $50,000

Northeast

29.8%

36.7%

15.4%

12.2%

5.9%

Midwest

41.4%

39.4%

14.6%

3.5%

1.0%

South

30.3%

39.9%

22.0%

7.9%

0.0%

West

25.3%

38.2%

19.8%

12.0%

4.6%

Since the onset of the COVID-19 pandemic, have you temporarily stopped making credit card payments?

Yes

No

Percentage of respondents

30.7%

69.3%

Since the onset of the COVID-19 pandemic, have you stopped temporarily making credit card payments? By Generation

Yes

No

Ages 18-24

57.0%

43.0%

Ages 25-39

39.2%

60.8%

Ages 40-54

21.0%

79.0%

Ages 55-74

17.3%

82.7%

Ages 75+

40.0%

60.0%

Since the onset of the COVID-19 pandemic, have you stopped temporarily making credit card payments? By Region

Yes

No

Northeast

31.6%

68.4%

Midwest

19.7%

80.3%

South

29.1%

70.9%

West

42.9%

57.1%

Do you regularly carry credit card debt month-to-month?

Percentage of respondents

Always

35.1%

More than once per year

17.0%

Once per year

11.6%

Almost never

11.2%

Never

25.1%

Do you regularly carry credit card debt month-to-month? By Generation

Always

More than once per year

Once per year

Almost never

Never

Ages 18-24

45.0%

25.8%

19.2%

2.5%

7.5%

Ages 25-39

32.7%

19.9%

9.9%

11.0%

26.5%

Ages 40-54

33.9%

20.2%

7.0%

11.6%

27.3%

Ages 55-74

32.8%

10.1%

6.8%

17.2%

33.1%

Ages 75+

40.7%

9.9%

34.1%

3.3%

12.1%

Do you regularly carry credit card debt month-to-month? By Region

Always

More than once per year

Once per year

Almost never

Never

Northeast

41.0%

16.5%

7.4%

10.6%

24.5%

Midwest

28.3%

19.2%

9.1%

9.6%

33.8%

South

38.2%

14.8%

13.1%

12.9%

21.0%

West

29.8%

20.2%

14.7%

9.6%

25.7%

Methodology: Data was collected Oct. 1-20, 2021, from 1,022 Americans over the age of 18, using a mixed mode sample of online, cell phone and telephone participants. All respondents interviewed in this study were part of either a fully representative sample using mixed mode random stratified probabilistic sampling and a non-probability panel sample. The credibility interval for the sample is +/- 3.065% in 19 of 20 cases.

Getting out of debt isn’t one-size-fits-all. There are dozens of private and government programs, and each one works best under certain circumstances. See how those options might affect you.

Step 1

How much do you owe?

$25,000

Pros and Cons

Let Debt.com Help You Choose the Best Plan

Talk to a debt relief specialist to weigh your options.

Minimum payment calculation assumes an APR of 24% on your credit card debt and each monthly payment is 3% of total amount.

Debt Consolidation

Assumes a loan APR of 16.5% over a 5- year term.

Debt Management Program

Average Interest Rate in a DMP is 8%. Actual interest rates will vary by consumer and creditor.

A DMP might be able to reduce your interest rates and late fees allowing you to pay off your credit card debt quicker (since more payments are applied to your principal balances, saving you lots of money in the long run). To complete the program, you must make on-time payments each month. Late or missed payments may cause your program to be canceled and in that event, this estimate would not apply to you.

Debt Settlement

Rates and terms vary by consumer and creditor. Debt settlement may negatively impact your credit score.

*Debt settlement fees vary by program and state.

Our Site uses cookies and pixels for compliance, user interactions recording, and relevant marketing services. 3rd-party cookies and pixels may share information with 3rd-party associates. Essential cookies cannot be rejected. By taking No Action, clicking the "[X]" or "ACCEPT ESSENTIAL COOKIES" you are accepting Essential Cookies and Pixels. To accept all cookies and pixels click "ACCEPT ALL COOKIES". By using the Site, you agree you read and accepted our Privacy Policy, Terms of Use, and Arbitration Agreements.