Debt.com’s writers are journalists, personal finance experts, and certified credit counselors. Their advice about money – how to make it, how to save it, and how to spend it – is based on, collectively, a century of personal finance experience. They’ve been featured in media outlets ranging from The New York Times to USA Today, from Forbes to FOX News, and from MSN to CBS.

Credit Card Survey: Inflation is Still Contributing to Debt

One in three Americans need credit cards to make ends meet – and many are maxed out.

For the second consecutive year, our survey of 1,000 Americans shows that one in three need credit cards to make ends meet – and many are maxed out.

U.S. credit card balances have ballooned since the worldwide inflation surge began in March 2021. According to the Federal Reserve, Americans owe a record-high $1.21 trillion on credit cards. Debt.com’s latest research shows how that affects their credit card usage:

32%: Have maxed out their credit cards

37%: Need their credit cards to make ends meet

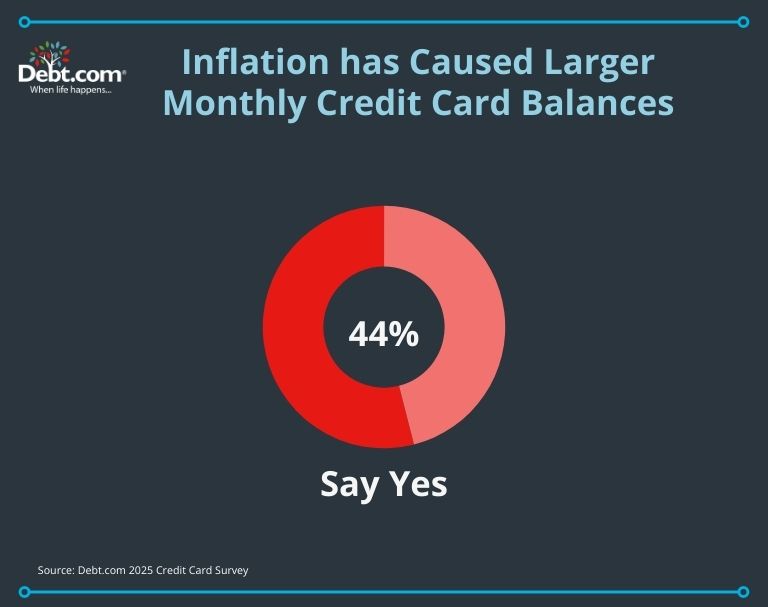

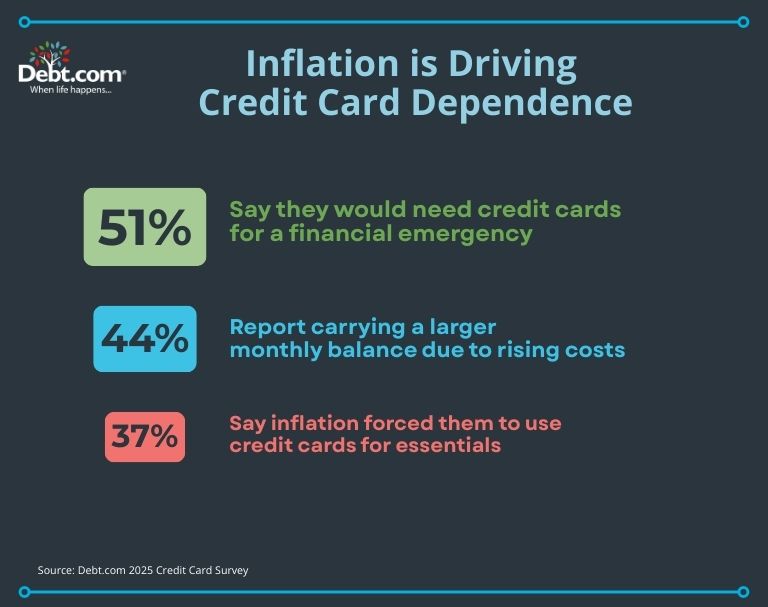

44%: Caused them to carry a larger monthly balance

Those who have already maxed out their cards are most vulnerable. Eight in ten “would need to rely on credit card(s) if faced with a financial emergency.” Just over 23% of them already owe more than $20,000.

Key findings

More than 1 in 3 (37%) of all survey respondents say “price increases from inflation caused them to use credit cards to make ends meet.” That includes 43% of Millennials and 41% of Gen Xers.

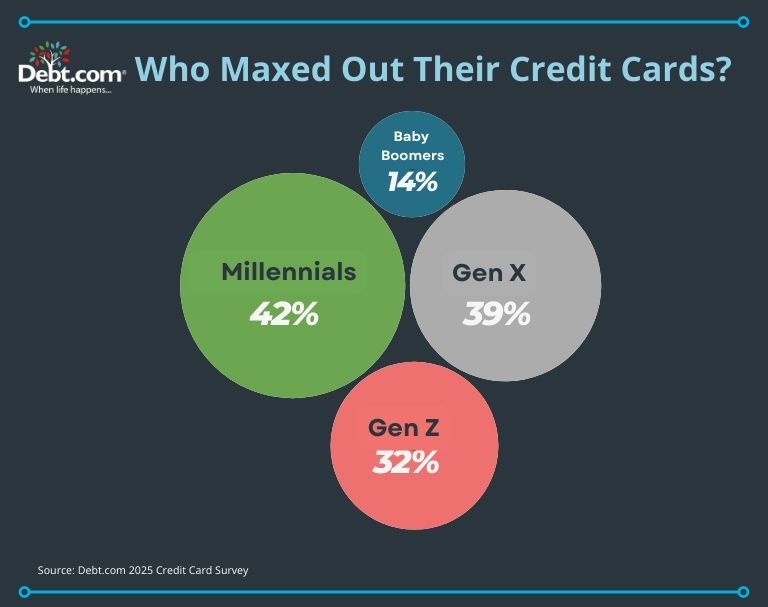

32% report having maxed out their credit cards in recent years. This group includes 32% Gen Z, 42% Millennials, 39% Gen Xers, and 14% Baby Boomers.

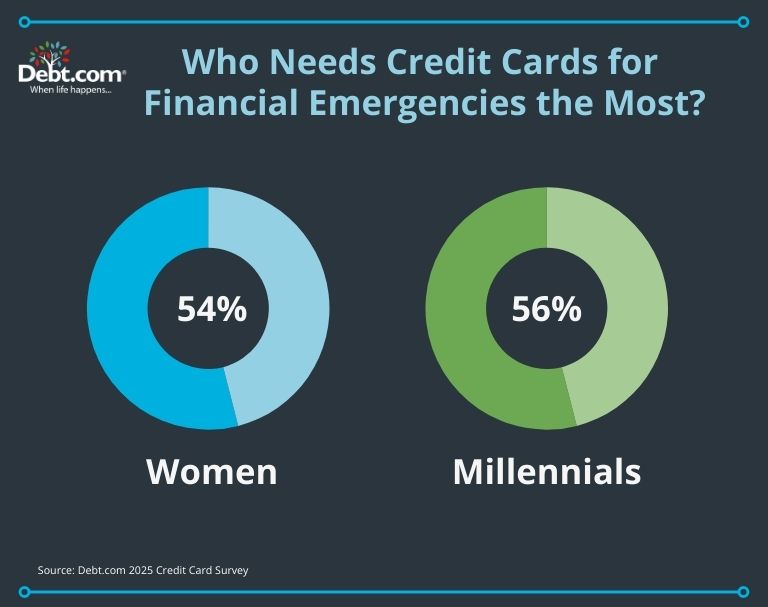

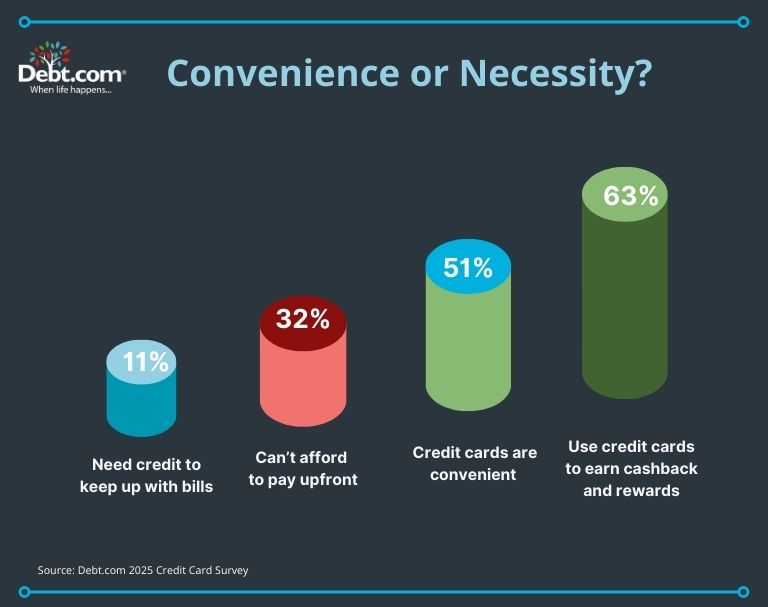

Over half (51%) of all respondents need credit cards to pay for a financial emergency. 56% are Millennials, and over half (54%) are women.

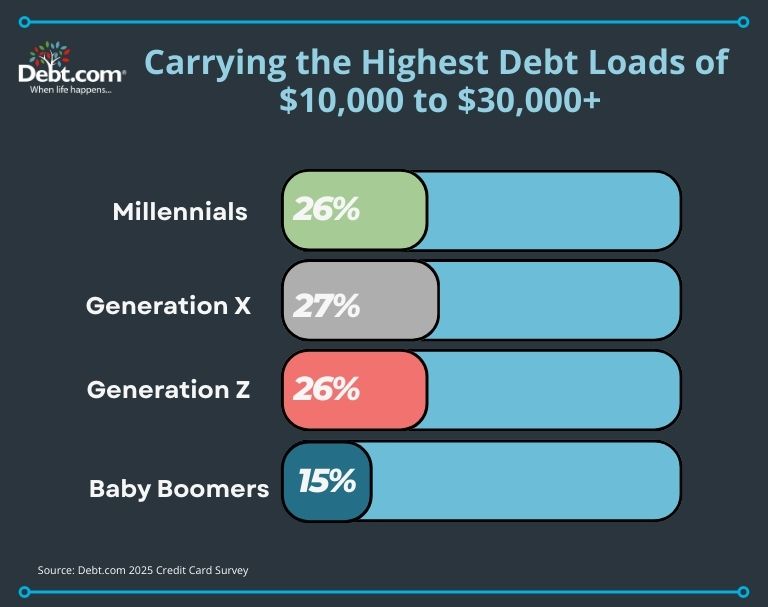

44% say inflation has “caused them to carry a larger monthly credit card balance.” Of those respondents, 39% have at least $10,000 to $20,000 of credit card debt. That includes 26% of Millennials.

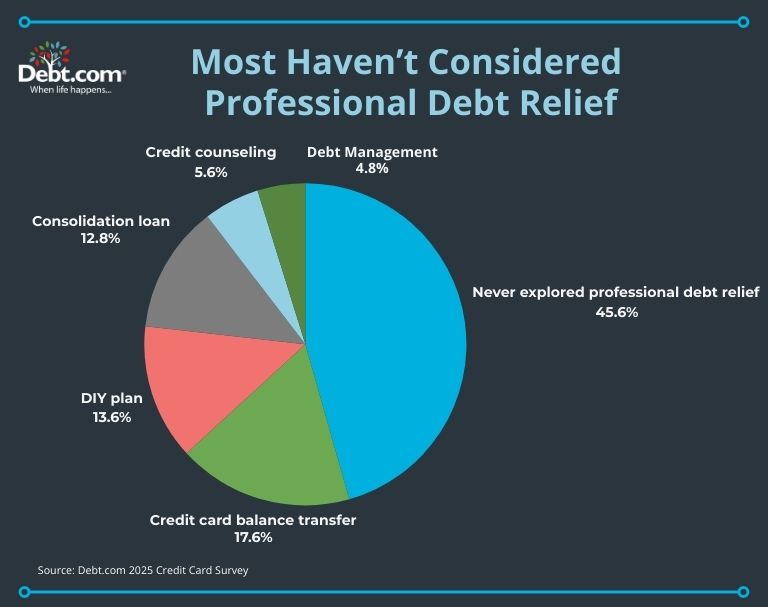

57% of all respondents have never considered Do-It-Yourself or professional credit card debt solutions like debt management and settlement programs – most of whom (74%) are Baby Boomers.

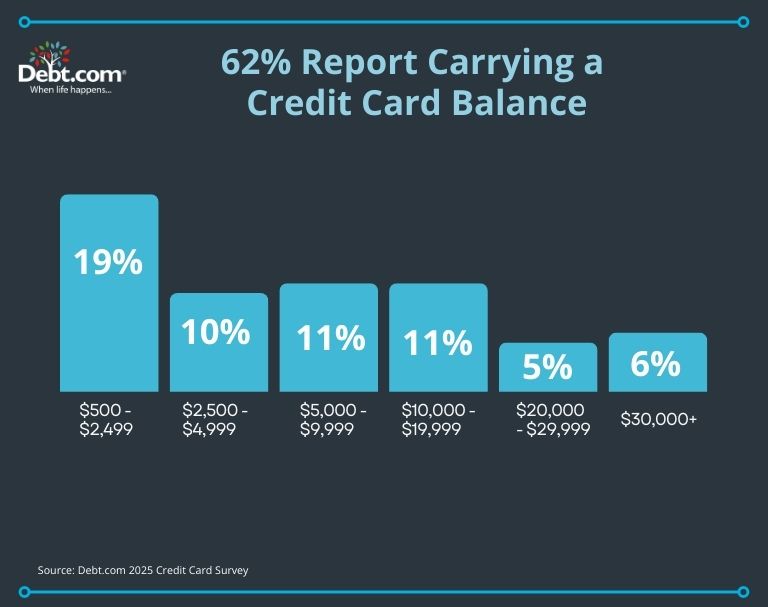

Carrying a balance is more common than not – with nearly 62% of people owing money on their credit cards. Over 1 in 5 owe $10,000 or more, highlighting the growing credit card debt burden.

High credit card debt isn’t limited by age. Gen Z, Millennials, and Gen X are neck and neck when it comes to carrying balances over $10,000. The exception is Baby Boomers, who are in or approaching retirement age.

Maxing out credit cards is a challenge many face – Millennials tend to hit their credit limits more often. From everyday expenses to rising costs, credit limits are being pushed as people try to keep up.

More than half of all respondents say they need credit cards to pay for a financial emergency.

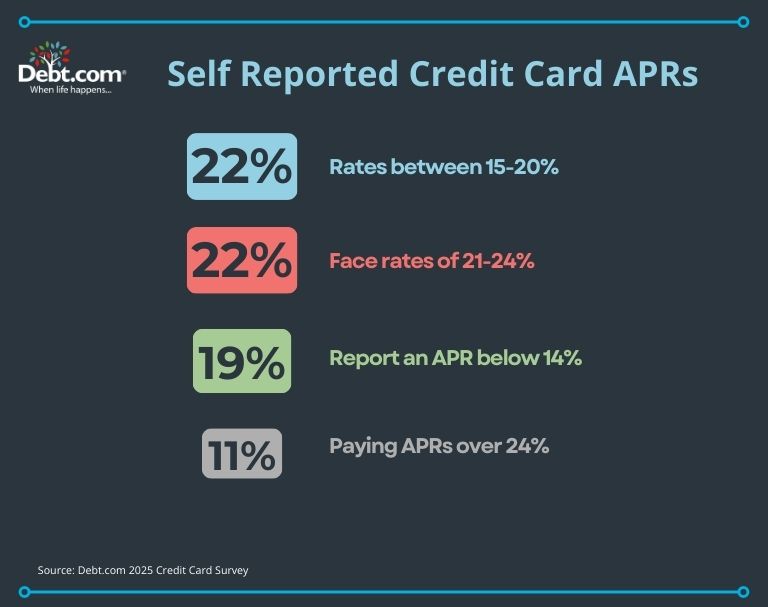

Interest rates matter – but not everyone knows what they’re paying. Despite climbing interest rates, 27% of respondents didn’t know their credit card APR.

When it comes to managing debt, most people go it alone or don’t explore options at all. A small percentage seek professional help like credit counseling or debt settlement. Financial solutions exist, but awareness is key.

Credit cards serve many purposes. Many people use them for rewards or convenience. But for others, it’s about survival covering purchases and staying current with bills.

More than 4 in 10 people say their balances increased due to higher costs of good

Rising prices are pushing people to rely on credit cards – and inflation is turning high APR debt into lifelines.

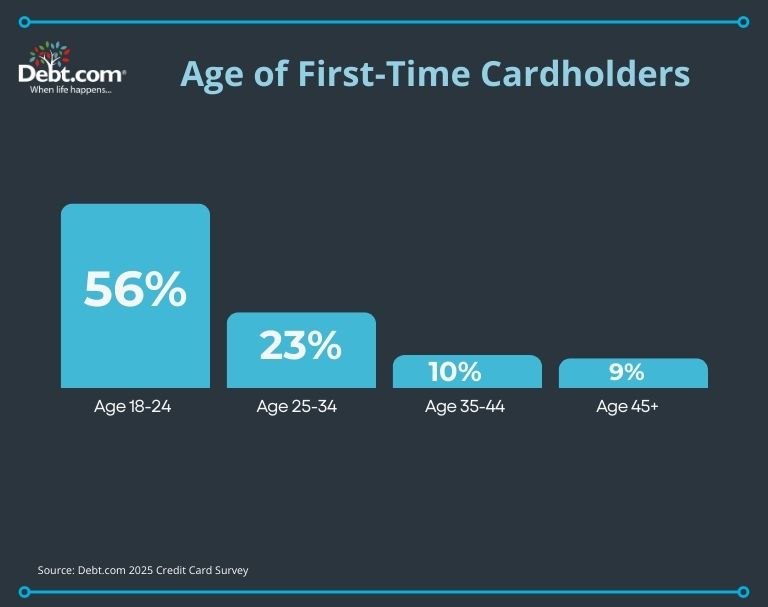

Most people start their credit journey at a young age, getting a credit card before they turn 25 years old. Building good habits early can make all the difference, but it also means young adults need the tools and knowledge to manage credit wisely.

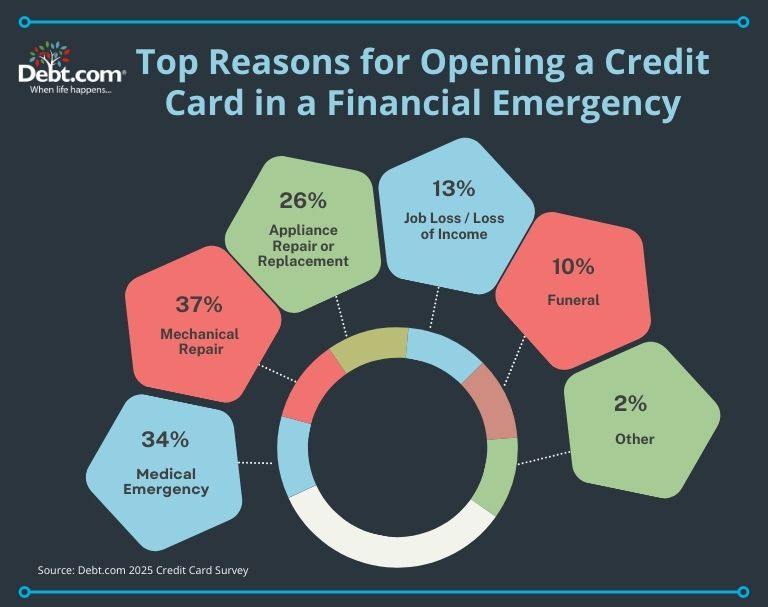

When unexpected expenses strike, many turn to credit cards. Auto repairs, medical bills, and appliance breakdowns top the list of emergencies that lead people to open a credit card – often out of necessity, not choice.

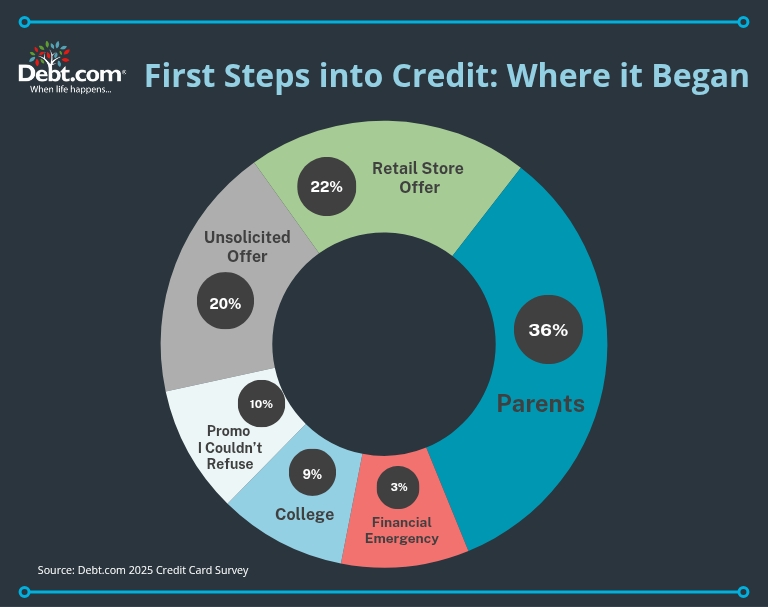

From parents to promotions, the path to a first credit card varies. Over one-third of people get their first card with help from family, while others take the plunge due to offers, emergencies, or tempting promotions.

Click here for full survey results

At what age did you get your first credit card?

Under 18

0%

18-24

55.98%

25-34

22.62%

35-44

9.62%

45-54

5.72%

55-64

1.91%

65+

1.73%

N/A

2.43%

Who introduced you to your first credit card?

Parent

35.86%

Unsolicited offer

20.09%

Retail store offer

21.98%

School (College credit card)

9.37%

Financial emergency

2.79%

The credit card company ran a promotion I wanted more than the card

9.91%

Which financial emergency did you charge on a credit card?

Medical emergency

34.32%

Mechanic

36.94%

Appliance repair

25.95%

Funeral

10.18%

Job loss

13.06%

I did not open a credit card due to an emergency

35.41%

Other

2.07%

What is your total credit card debt?

More than $30,000

6.49%

$20,000 to $29,999

5.32%

$10,000 to $19,999

11.44%

$5,000 to $9,999

10.63%

$2,500 to $4,999

9.82%

$500 to $2,499

19.01%

I have a credit card but don’t carry credit card debt

37.30%

Do you know what your average credit card APR is?

0-14%

18.83%

15%-20%

21.53%

21%-24%

22.34%

Over 24%

10.72%

I don’t know

26.58%

Why do you use credit cards?

They’re the most convenient form of payment

50.99%

I earn cashback and rewards

63.24%

It’s easy to dispute fraudulent charges that I can’t with a debit card

36.94%

Credit cards allow me time to make purchases I can’t afford now

31.71%

I couldn’t survive and pay my bills right now without credit cards

10.54%

Other

5.59%

Have you maxed out your credit cards in recent years due to inflation and increased interest rates?

Yes

31.98%

No

68.02%

Have price increases from inflation made you use your credit cards to make ends meet?

Yes

37.48%

No

62.52%

Has inflation caused you to carry a larger monthly credit card balance?

Yes

43.96%

No

56.04%

Would you need to rely on your credit card(s) if faced with a financial emergency?

Yes

50.63%

No

49.37%

Do you know your FICO score?

Yes

78.65%

No

21.35%

What FICO credit score range do you fit in?

Excellent: 800 to 850

31.08%

Very good: 740 to 799

27.48%

Good: 670 to 739

16.85%

Fair: 580 to 669

9.46%

Poor: 300 to 579

3.78%

I don’t know my FICO score:

11.35%

Have you considered using any of the following solutions to help with your credit card debt?

Yes, DIY plans like “debt snowball” and “debt avalanche”

16.85%

Yes, a credit card balance

22.07%

Yes, a consolidation loan

16.04%

Yes, credit counseling

7.03%

Yes, debt settlement

5.68%

No

56.94%

For 2024 survey results, click here

At what age did you get your first credit card?

18-24

55.71%

25-34

24.37%

35-44

12.48%

45-54

4.45%

55-64

1.26%

65+

1.74%

Who introduced you to your first credit card?

Parent(s)

32.21%

Unsolicited offer

21.28%

Retail store offer

25.82%

School (College credit card)

12.19%

Financial emergency

8.51%

Select which financial emergency you’ve needed to charge on a credit card in recent years.

Medical emergency

65.12%

Mechanic (Auto repair)

44.19%

Appliance repair or replacement

52.33%

Funeral expenses

24.42%

Job loss / loss of income

27.91%

What is your total credit card debt?

More than $30,000

5.16%

$20,000 to $29,999

5.56%

$10,000 to $19,999

10.91%

$5,000 to $9,999

11.81%

$2,500 to $4,999

14.29%

$500 to $2,499

52.28%

Do you know what your average credit card APR is?

0-14%

29.07

15-20%

35.71%

20-24%

25.79%

Over 24%

9.42%

Why do you use credit cards?

Strongly Disagree

Disagree

Neither Agree Nor Disagree

Agree

Strongly Agree

They’re convenient.

4.17%

4.27%

18.25%

41.67%

31.65%

I earn cashback and rewards.

5.75%

6.35%

13.00%

36.90%

38.00%

It’s easy to dispute fraud.

5.85%

6.75%

23.12%

38.00%

26.29%

They allow me time to make purchases I can’t afford.

19.64%

11.31%

18.95%

32.54%

17.56%

I can’t pay my bills without credit them.

35.42%

21.13%

15.97%

16.67%

10.81%

Have you maxed out your credit cards in recent years while inflation and interest rates have increased?

Yes

34.72%

No

65.28%

Have price increases from inflation made you use your credit cards to make ends meet?

Yes

45.34%

No

54.66%

Has inflation caused you to carry a larger monthly credit card balance?

Yes

51.39%

No

48.61%

Would you need to rely on your credit card(s) if faced with a financial emergency?

Yes

55.46%

No

44.54%

Do you know your credit score?

Yes

80.74%

No

19.26%

What credit score range do you fit in?

Excellent: 800 to 850

40.32%

Very good: 740 to 799

29.59%

Good: 670 to 739

17.63%

Fair: 580 to 669

10.36%

Poor: 300 to 579

2.10%

Have you considered using any of the following solutions to help with your credit card debt?

Yes, DIY plans like “debt snowball” and “debt avalanche” methods

11.17%

Yes, a credit card balance transfer

18.84%

Yes, a consolidation loan

13.96%

Yes, credit counseling

12.56%

Yes, debt settlement

9.97%

No

58.42%

For 2023 survey results, click here

What is your total credit card debt?

More than $30,000

5.60%

$20,000 to $29,999

6.07%

$10,000 to $19,999

9.58%

$5,000 to $9,999

11.86%

$2,500 to $4,999

11.39%

$500 to $2,499

30.27%

N/A

25.24%

Do you know what your average credit card APR is?

0-14%

16.86%

15-20%

22.10%

21-24%

24.19%

Over 24%

9.24%

I don’t know

27.62%

Have you maxed out your credit cards due to inflation and rising interest rates?

Yes

31.05%

No

68.95%

Has inflation caused you to carry a larger monthly credit card balance?

Yes

48.67%

No

51.33%

Other than inflation, have any of these reasons added to having to take on more debt?

Reduced income

27.52%

Loss of job

13.90%

Death of a family member

7.43%

Divorce or separation

6.38%

Medical issues

17.43%

N/A

53.52%

Have you considered any of the following solutions to help with your credit card debt?

Yes, DIY plans like “debt snowball” or “debt avalanche” methods

14.18%

Yes, a credit card balance transfer

18.97%

Yes, a consolidation loan

15.90%

Yes, credit counseling

6.99%

Yes, debt settlement

5.94%

No

58.14%

For 2021 survey results, click here

Do you use credit cards

Yes

10.26%

No

89.47%

When you’re shopping for a credit card, what features do you look for?

Best rewards

16.47%

More cash back

18.96%

Lower interest rate

64.57%

How many credit cards do you have?

More than 12

2.32%

Nine to 12

4.03%

Six to eight

12.30%

Two

22.68%

One

23.69%

Three to five

34.98%

How many credit cards do you actively use?

More than 12

0.20%

Nine to 12

0.50%

Six to eight

2.83%

Three to five

25.93%

Two

26.84%

One

43.69%

Have Americans learned to use credit cards sparingly since the pandemic?

I don’t know

25.08%

As soon as the pandemic ends, we’ll run up bills at restaurants and retailers

33.40%

I believe we’ve learned how much interest and fees cost. We’ll permanently cut back.

41.52%

What is your total credit card debt?

More than $20,000

10.53%

More than $10,000

10.93%

$5,001 to $10,000

12.84%

$2,501 to $5,000

16.05%

$501 to $2,500

17.85%

$0 to $100

20.96%

What do you think the average interest rates on your credit cards are?

0 to 5%

8.03%

6% to 9%

10.84%

10% to 12%

12.45%

13% to 15%

17.17%

16% to 20%

30.02%

More than 20%

21.49%

Do you ever hit the limit on your credit cards?

I have hit a limit in the past six months

6.26%

I have hit a limit in the past three months

7.68%

I hit my credit limit monthly

8.79%

I have hit a limit in the past year

19.49%

I never or rarely hit my credit limits

57.78%

Have you ever used a balance transfer to consolidate debt?

Yes

37.07%

No

62.93%

On the card you transferred the balance from, did you continue to use that card for purchases?

Yes

42.12%

No

57.88%

Did you pay off the balance transfer before the teaser rate expired?

Yes

61.10%

No

38.90%

When was the last time you signed up for a new credit card?

Yesterday

1.91%

Last month

8.79%

In the past 13 to 18 months

11.23%

In the past seven to 12 months

13.56%

In the past two to six months

15.25%

It’s been over five years

22.35%

It’s been over two years

26.91%

Which credit card company has the best customer service?

Wells Fargo

1.91%

Citibank

4.13%

Bank of America

4.56%

American Express

9.64%

Chase

11.97%

Discover

14.72%

Capital One

23.73%

N/A

23.34%

Which credit card company has the worst customer service?

Citibank

3.50%

Discover

3.61%

American Express

4.56%

Chase

5.52%

Capital One

6.79%

Wells Fargo

11.25%

Bank of America

13.16%

N/A

31.59%

Have you ever used a credit monitoring service?

Yes

39.26%

No

60.74%

Do you believe that the information in your credit report is accurate?

Yes

78.73%

No

21.27%

When was the last time you reviewed your credit report?

Never

5.93%

In the past five years

6.24%

In the past two years

10.48%

In the past year

18.10%

In the past six years

59.26%

Do you know that you can receive a free annual credit report guaranteed by federal law?

Yes

84.44%

No

15.56%

For 2019 survey results, click here

Do you use credit cards?

Yes

84.56%

No

15.44%

When you’re shopping for a credit card, what features do you look for?

Lower interest rate

68.37%

Most cash back

14.33%

Best rewards

17.30%

How many credit cards do you have?

1

15.35%

2

20.74%

3-5

41.58%

6-8

15.35%

9-12

3.81%

More than 12

3.16%

How many credit cards do you actively use?

1

31.94%

2

32.50%

3-5

31.56%

6-8

3.35%

9-12

0.19%

More than 12

0.47%

What is your total current credit card debt?

$0-$100

11.32%

$101-$500

11.23%

$501-$2,500

21.51%

$2,501-$5,000

15.38%

$5,001-$10,000

18.02%

More than $10,000

13.21%

More than $20,000

9.34%

What do you think is the average interest rates on your credit cards?

0-5%

6.33%

6%-9%

8.79%

10%-12%

13.42%

13%-15%

20.32%

16%-20%

26.47%

More than 20%

24.67%

Do you ever hit the credit limit on your credit cards?

I never or rarely hit my credit limits

49.01%

I have hit a limit in the past year

16.84%

I have hit a limit in the past 6 months

8.23%

I have hit a limit in the past 3 months

14.29%

I hit my credit limit monthly

11.64%

Have you ever used a balance transfer offer to consolidate debt?

Yes

38.45%

No

61.55%

On the card that you transferred the balance from, did you continue to use that card for purchases?

Yes

41.23%

No

58.77%

Did you pay off the balance transfer before the teaser rate expired?

Yes

61.04%

No

38.96%

When was the last time you signed up for a new credit card?

Yesterday

1.13%

Last month

7%

In the past 2-6 months

13.12%

In the past 7-12 months

13.45%

In the past 13-18 months

15.06%

It’s been over 2 years

25.68%

It’s been over 5 years

24.56%

Which credit card company has the best customer service?

Capital One

25.41%

Chase

12.91%

Discover

17.21%

Citibank

4.95%

American Express

7.55%

Wells Fargo

5.11%

N/A

31.98%

Do you use credit monitoring services?

Yes

59.66%

No

40.34%

Do you believe the information in your credit report is accurate?

Yes

53.59%

No

12.99%

Unsure

33.42%

When was the last time you reviewed your credit report?

In the past six months

54.07%

In the past year

17.91%

In the past two years

10.76%

In the past five years

11.18%

Never

6.08%

Do you know that you can receive a free annual credit report guaranteed by federal law?

Yes

83.07%

No

16.93%

For full 2018 survey results, click here

Do you use credit cards?

Yes

84.86%

No

15.14%

When you’re shopping for a credit card, what features do you look for?

Lower interest rate

58.11%

Most cash back

20.28%

Best rewards

21.61%

How many credit cards do you have?

1

13.46%

2

22.97%

3-5

43.95%

6-8

13.15%

9-12

3.99%

More than 12

2.48%

How many credit cards do you actively use?

1

33.01%

2

34.93%

3-5

28.32%

6-8

2.71%

9-12

0.74%

More than 12

0.28%

What is your total current credit card debt?

$0-$100

21.95%

$101-$500

8.89%

$501-$2,500

8.79%

$2,501-$5,000

15.62%

$5,001-$10,000

10.25%

More than $10,000

13.21%

More than $20,000

9.34%

What do you think is the average interest rates on your credit cards?

0-5%

7.37%

6%-9%

10.58%

10%-12%

16.98%

13%-15%

21.60%

16%-20%

26.52%

More than 20%

16.95%

Do you ever hit the credit limit on your credit cards?

I never or rarely hit my credit limits

64.20%

I have hit a limit in the past year

12.57%

I have hit a limit in the past 6 months

4.98%

I have hit a limit in the past 3 months

9.95%

I hit my credit limit monthly

8.30%

Have you ever used a balance transfer offer to consolidate debt?

Yes

35.20%

No

64.80%

On the card that you transferred the balance from, did you continue to use that card for purchases?

Yes

67.66%

No

32.34%

Did you pay off the balance transfer before the teaser rate expired?

Yes

67.66%

No

32.34%

When was the last time you signed up for a new credit card?

Yesterday

0.74%

Last month

6.40%

In the past 2-6 months

11.08%

In the past 7-12 months

11.72%

In the past 13-18 months

11.92%

It’s been over 2 years

23.05%

It’s been over 5 years

35.07%

Which credit card company has the best customer service?

Capital One

25.41%

Chase

12.91%

Discover

17.21%

Citibank

4.95%

American Express

7.55%

Wells Fargo

5.11%

N/A

31.98%

Do you use credit monitoring services?

Yes

46.48%

No

53.52%

Do you believe the information in your credit report is accurate?

Yes

57.46%

No

10.69%

Unsure

31.85%

When was the last time you reviewed your credit report?

In the past six months

50.26%

In the past year

20.41%

In the past two years

11.43%

In the past five years

12.14%

Never

5.76%

Do you know that you can receive a free annual credit report guaranteed by federal law?

Yes

85.99%

No

14.03%

Methodology: Debt.com surveyed 1,000 Americans about their credit card usage and debt. People responded from all 50 states and Washington, DC, and were aged 18 and above. Responses were collected through SurveyMonkey. The survey was conducted on March 06, 2025.

Getting out of debt isn’t one-size-fits-all. There are dozens of private and government programs, and each one works best under certain circumstances. See how those options might affect you.

Step 1

How much do you owe?

$25,000

Pros and Cons

Let Debt.com Help You Choose the Best Plan

Talk to a debt relief specialist to weigh your options.

Minimum payment calculation assumes an APR of 24% on your credit card debt and each monthly payment is 3% of total amount.

Debt Consolidation

Assumes a loan APR of 16.5% over a 5- year term.

Debt Management Program

Average Interest Rate in a DMP is 8%. Actual interest rates will vary by consumer and creditor.

A DMP might be able to reduce your interest rates and late fees allowing you to pay off your credit card debt quicker (since more payments are applied to your principal balances, saving you lots of money in the long run). To complete the program, you must make on-time payments each month. Late or missed payments may cause your program to be canceled and in that event, this estimate would not apply to you.

Debt Settlement

Rates and terms vary by consumer and creditor. Debt settlement may negatively impact your credit score.

*Debt settlement fees vary by program and state.

Our Site uses cookies and pixels for compliance, user interactions recording, and relevant marketing services. 3rd-party cookies and pixels may share information with 3rd-party associates. Essential cookies cannot be rejected. By taking No Action, clicking the "[X]" or "ACCEPT ESSENTIAL COOKIES" you are accepting Essential Cookies and Pixels. To accept all cookies and pixels click "ACCEPT ALL COOKIES". By using the Site, you agree you read and accepted our Privacy Policy, Terms of Use, and Arbitration Agreements.