Debt.com’s writers are journalists, personal finance experts, and certified credit counselors. Their advice about money – how to make it, how to save it, and how to spend it – is based on, collectively, a century of personal finance experience. They’ve been featured in media outlets ranging from The New York Times to USA Today, from Forbes to FOX News, and from MSN to CBS.

Medical Debt Survey: 9 in 10 Americans with Medical Debt Say it Shouldn’t Hurt Their Credit.

More than half say past-due medical bills have damaged their credit scores.

In January 2025, the Consumer Financial Protection Bureau (CFPB) finalized a rule to remove medical debt from credit reports. But that rule – and the agency behind it – are under political scrutiny, with Republican lawmakers pushing to dismantle both.

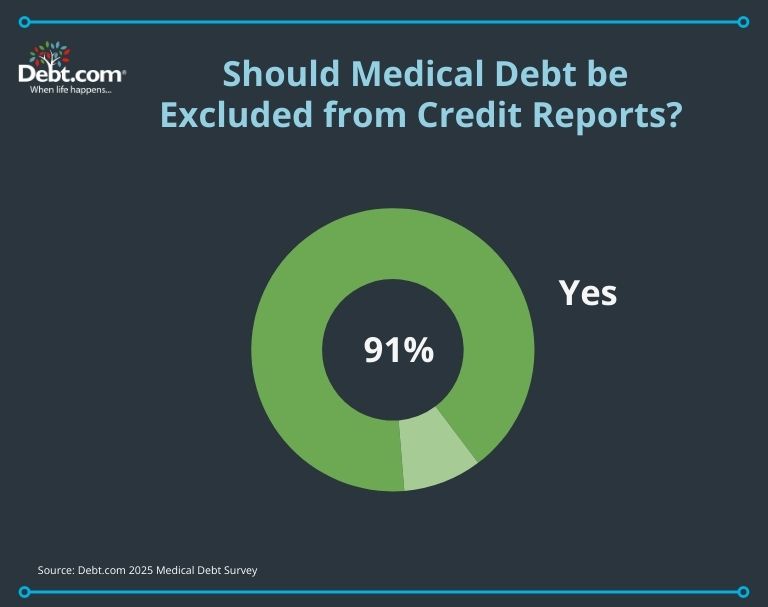

Debt.com’s latest survey suggests most Americans support the CFPB’s move. In a national poll, 91% with medical debt agree that it should be excluded from credit reports.

When asked why, 30% said: “Medical debt is often unavoidable and doesn’t reflect financial responsibility.” Among the 9% who disagreed, nearly 1 in 5 said removing the debt might encourage people to avoid paying their medical bills.

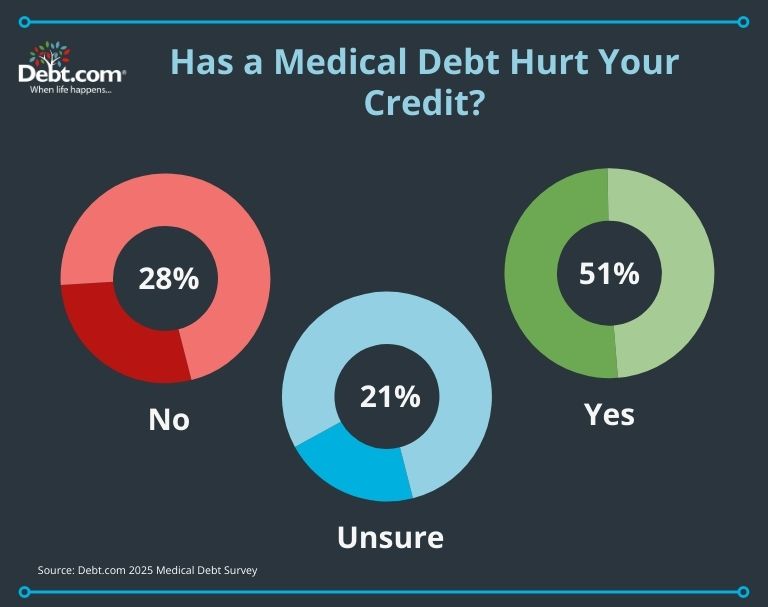

More than half (51%) say a “past medical debt has hurt their credit.” Three in ten say by 50 to 100 points, with 14% reporting a credit score drop of more than 100 points.

The survey also revealed how widespread medical debt remains – and how damaging it can be:

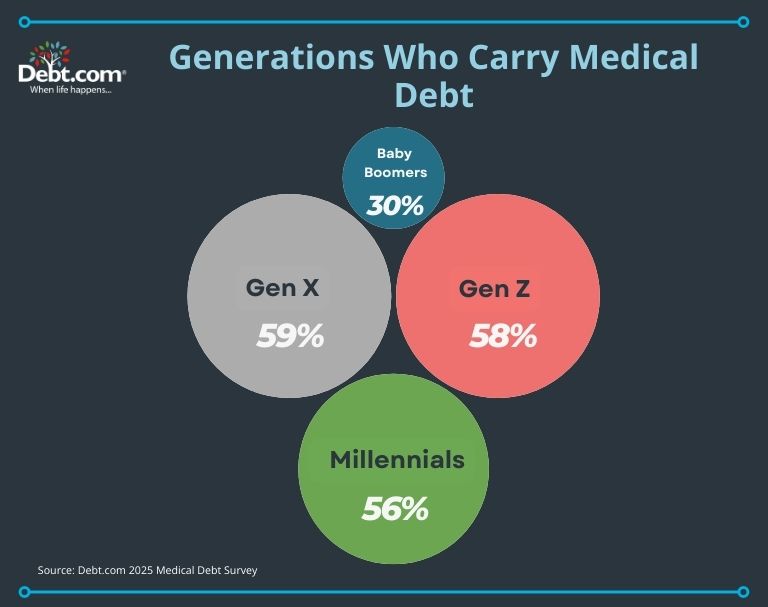

Half of Americans say they currently have outstanding medical bills or unpaid medical debt

59% say they’ve skipped or delayed medical care because of what they already owe

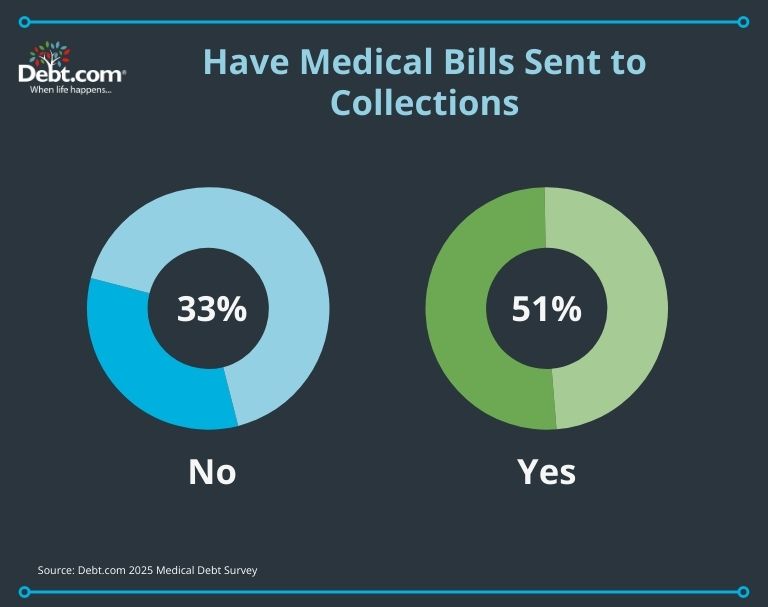

51% of those with medical debt say their accounts have been sent to collections

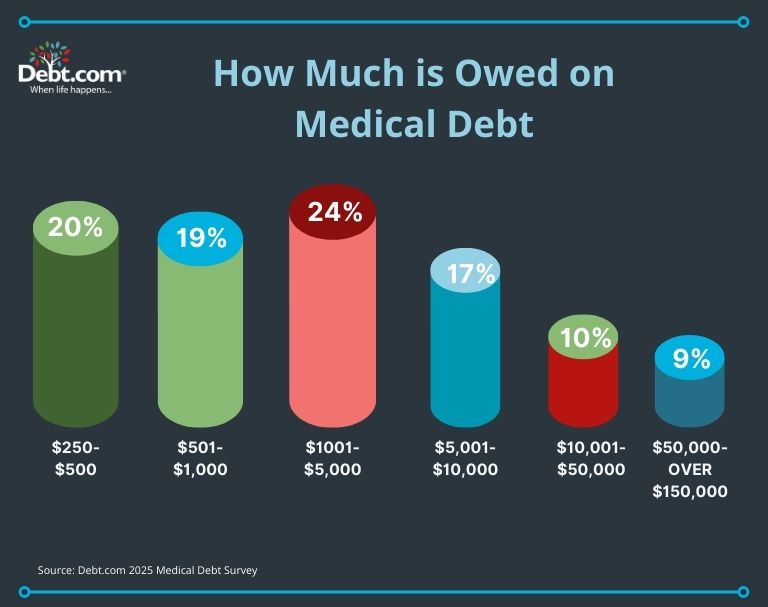

20% owe $10,000 or more

9% owe $50,000 or more

Over the past six years that Debt.com has conducted this survey, medical debt has remained high. Nearly 1 in 5 respondents have consistently owed more than $10,000 in medical bills.

In January 2025, the Consumer Financial Protection Bureau (CFPB) finalized a rule to remove medical debt from credit reports. Some Republican lawmakers are now challenging that rule, along with efforts to dismantle the agency itself.

Medical debt is not uncommon, nor is its impact on credit. More than 51% of people polled say they have medical debt, and 51% say a “past medical debt has hurt their credit.” As lawmakers and agency officials debate the role of medical debt in credit reporting, Americans continue to feel the pressure.

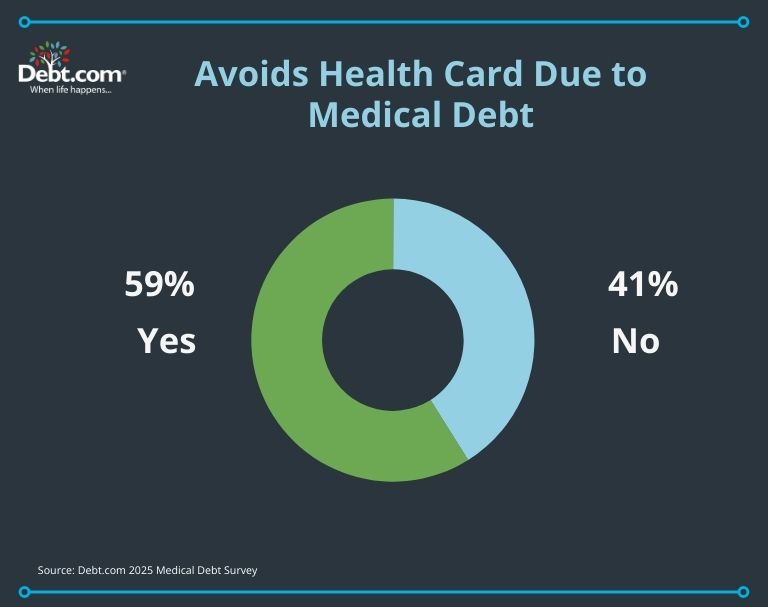

More than 59% of those with medical debt say they’ve been avoiding medical care because of their debt, further highlighting the burden this type of debt can place on people’s lives.

Half of all respondents say they currently have medical debt – but Gen X is the most affected, with 59% reporting outstanding medical bills. Gen Z follows closely at 58%, and Millennials aren’t far behind at 56%.

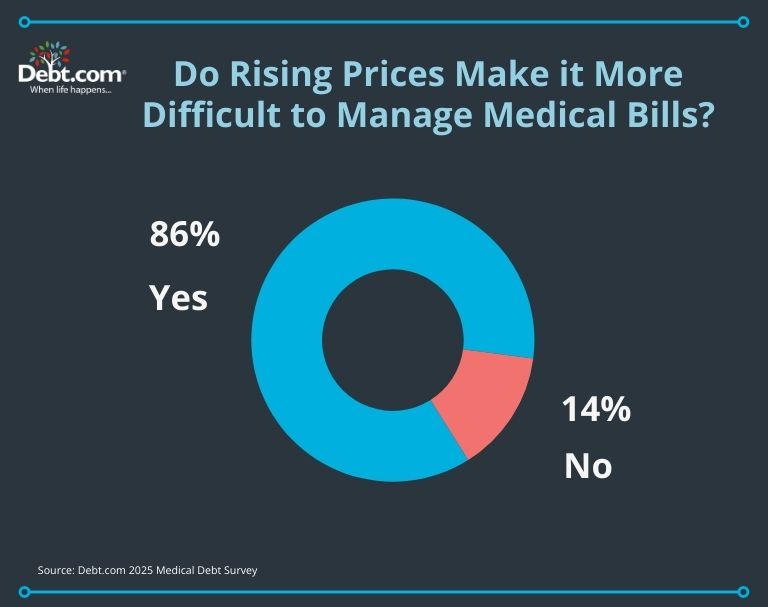

Amid ongoing inflation, Americans with medical debt are finding it harder than ever to pay it off.

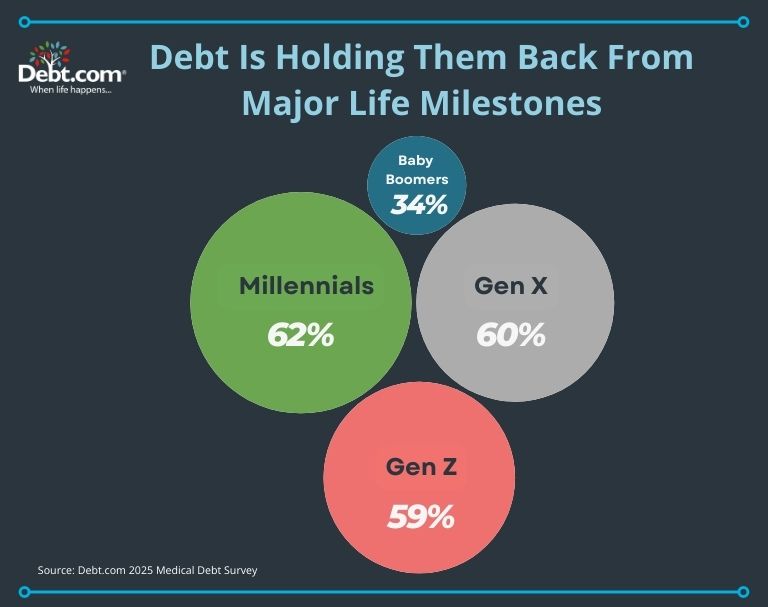

Medical debt is disrupting goals like higher education, marriage, homeownership, or starting a family across all age groups – but Millennials are feeling the impact most.

Click here for full survey results

Do you have outstanding medical bills or medical debt?

Yes

51.32%

No

48.68%

Have your medical bills been sent to collections?

Yes

51.29%

No

32.66%

Unsure

16.05%

How much do you owe?

$250-$500

19.77%

$501-$1,000

19.48%

$1,001-$5,000

24.36%

$5,001-$10,000

16.62%

$10,001-$50,000

10.32%

$50,001-$100,000

3.15%

$100,001-$150,000

3.15%

More than $150,000

3.15%

Have you been avoiding medical care because of your debt?

Yes

59.31%

No

40.69%

Has a past medical debt hurt your credit?

Yes

51.00%

No

27.79%

Unsure

21.20%

If yes, how much did your credit score change as a result of your medical debt?

Decreased by 50 points or less.

20.12%

Decreased by more than 50 points.

16.57%

Decreased by 50 to 100 points.

30.18%

Decreased by more than 100 points.

14.20%

My credit score was unaffected.

4.14%

I don’t know.

14.79%

What type of health insurance do you have?

Employer-provided

47.85%

Medicare or Medicaid

32.09%

Self-purchased through an exchange

12.89%

None

7.16%

What is the primary source of your medical debt?

Diagnostic tests

18.34%

Hospitalization

20.92%

Emergency room

20.63%

Outpatient services

13.47%

Doctor visits

11.46%

Dental care

5.44%

Prescription drugs

4.58%

Nursing home/long-term care

0.86%

Mental health services

1.43%

Pregnancy and childbirth

2.87%

Do you believe medical debt should be excluded from credit reports?

Yes

90.83%

No

9.17%

If yes, why?

Medical debt is often unavoidable and doesn’t reflect financial responsibility.

30.19%

It creates unnecessary stress and hinders recovery.

8.77%

It is often complex and inaccurate, leading to unfair credit impacts.

10.06%

All of the above

46.75%

Other

2.27%

N/A

1.95%

If no, why?

Medical debt is a legitimate debt and should be treated as such.

16.13%

Excluding it would encourage people to avoid paying their medical bills

22.58%

Credit reports should reflect all financial obligations for accurate risk assessment

12.90%

All of the above

19.35%

N/A

29.03%

Has inflation made it harder to pay your medical bills?

Yes

86.49%

No

13.51%

How did your insurance company respond to your medical bills?

Told me I received out-of-network care

31.32%

Denied my claim

28.45%

Other – N/A

40.23%

Have you tried to negotiate to lower the cost of your bills?

Yes, I tried to negotiate on my own.

51.72%

Yes, I used a medical bills advocate.

12.07%

No

36.21%

Were you successful in this negotiation?

Yes

47.67%

No

52.33%

Are you currently on a payment plan?

Yes

52.30%

No

47.70%

Is medical debt holding you back from future life goals (pursuing higher education, getting married, buying a home, starting a family, etc.)

Yes

56.61%

No

43.39%

How has your medical debt interrupted your finances? (select all that apply)

I had to withdraw all the money in my emergency fund.

35.63%

I had to withdraw money from my retirement account.

25.86%

I took out a HELOC on my home to pay my medical bills.

10.63%

I charged the medical debt on a credit card.

25.86%

My medical debt has caused me to go further into debt with credit cards and personal loans.

22.70%

I’ve had to pick up multiple jobs to pay the medical debt.

10.06%

I can’t see a doctor until I pay down more of my medical debt.

16.67%

For full 2024 survey results, click here

Do you have outstanding medical bills or medical debt?

Yes

66%

No

34%

Have your medical bills been sent to collections?

Yes

50%

No

39%

Unsure

12%

How much do you owe in medical debt?

$250-$500

36%

$501-$1,000

13%

$1,001-$5,000

15%

$5,001-$10,000

12%

$10,001-$50,000

7%

$50,001-$100,000

4%

$101,000-$150,000

8%

More than $150,000

6%

Have you been avoiding medical care because of your debt?

Yes

52%

No

48%

What type of health insurance do you have?

Employer-provided

50%

Medicare or Medicaid

36%

Self-purchased through an exchange

8%

None

5%

What is the primary source of your medical debt?

Diagnostic tests

26%

Hospitalization

18%

Emergency room

14%

Outpatient services

10%

Doctor visits

16%

Dental care

8%

Prescription drugs

5%

Nursing home/long-term care

1%

Has inflation made it harder to pay your medical bills?

Yes

79%

No

21%

How did your insurance company respond to your medical bills?

Told me I received out-of-network care

39%

Denied my claim

20%

Other – N/A

42%

Have you tried negotiating to lower the cost of your bills?

Yes, I tried to negotiate on my own

45%

Yes, I used a medical bills advocate

12%

No

43%

Were you successful in this negotiation?

Yes

47%

No

53%

Are you currently on a payment plan?

Yes

55%

No

45%

Is your medical debt holding you back from future life goals?

Yes

55%

No

45%

How has your medical debt interrupted your finances?

I had to withdraw all the money in my emergency fund

14%

I had to withdraw money from my retirement account

11%

I took out a HELOC on my home to pay my medical bills

6%

I charged the medical debt on a credit card

28%

My medical debt caused me to go further into debt with credit cards and personal loans

20%

I’ve had to pick up multiple jobs to pay the medical debt

9%

I can’t see a doctor until I pay down more of my medical debt

11%

For 2023’s full survey results, click here

Do you have outstanding medical bills or medical debt?

Yes

49.50%

No

50.50%

Have your medical bills been sent to collections?

Yes

31.54%

No

56.39%

Unsure

12.08%

How much do you owe in medical debt?

Less than $500

55.69%

$501-$1,000

11.68%

$1,001-$5,000

15.37%

$5,001-$10,000

6.29%

$10,001-$50,000

4.59%

$50,001-$100,000

2.20%

$101,000-$150,000

2.59%

More than $150,000

1.60%

Have you been avoiding medical care because of your debt?

Yes

33.63%

No

66.37%

What type of health insurance do you have?

Employer-provided

45.41%

Medicare or Medicaid

38.62%

Self-purchased through an exchange

8.78%

None

7.19%

What is the primary source of your medical debt?

Diagnostic tests

15.47%

Hospitalization

16.87%

Emergency room

16.67%

Outpatient services

10.18%

Doctor visits

21.06%

Dental care

10.988%

Prescription drugs

7.49%

Nursing home/long-term care

1.30%

Has inflation made it harder to pay your medical bills?

Yes

66.97%

No

33.03%

How did your insurance company respond to your medical bills?

Told me I received out-of-network care

22.26%

Denied my claim

14.47%

Other – N/A

63.27%

Have you tried negotiating to lower the cost of your bills?

Yes, I tried to negotiate on my own

29.64%

Yes, I used a medical bills advocate

11.08%

No

59.28%

Were you successful in this negotiation?

Yes

31.24%

No

68.76%

Are you currently on a payment plan?

Yes

35.53%

No

64.47%

For 2022’s full survey results, click here

Do you have outstanding medical bills or medical debt?

Yes

44.46%

No

55.54%

Have your medical bills been sent to collections?

Yes

28.41%

No

61.44%

Unsure

10.15%

How much do you owe in medical debt?

Less than $500

59.23%

$501-$1,000

33.21%

$1,001-$5,000

15.68%

$5,001-$10,000

5.35%

$10,001-$50,000

2.95%

$50,001-$100,000

2.03%

$101,000-$150,000

0.92%

More than $150,000

1.11%

Have you been avoiding medical care because of your debt?

Yes

27.68%

No

72.32%

What type of health insurance do you have?

Employer-provided

45.94%

Medicare or Medicaid

36.90%

Self-purchased through an exchange

10.89%

None

6.27%

What is the primary source of your medical debt?

Diagnostic tests

15.68%

Hospitalization

14.02%

Emergency room

15.68%

Outpatient services

11.07%

Doctor visits

21.22%

Dental care

11.25%

Prescription drugs

9.23%

Nursing home/long-term care

1.85%

Has inflation made it harder to pay your medical bills?

Yes

57.38%

No

42.62%

How did your insurance company respond to your medical bills?

Told me I received out-of-network care

21.22%

Denied my claim

10.70%

Other – N/A

68.08%

Have you tried negotiating to lower the cost of your bills?

Yes, I tried to negotiate on my own

26.38%

Yes, I used a medical bills advocate

8.12%

No

65.50%

Were you successful in this negotiation?

Yes

26.20%

No

73.80%

Are you currently on a payment plan?

Yes

29.15%

No

73.80%

For 2021’s full survey results, click here

Do you have outstanding medical bills or medical debt?

Yes

50.09%

No

49.91%

Have your medical bills been sent to collections?

Yes

45.86%

No

39.47%

Unsure

14.67%

How much do you owe in medical debt?

Less than $500

20%

$501-$1,000

23.26%

$1,001-$5,000

33.72%

$5,001-$10,000

12.02%

$10,001-$50,000

6.9%

$50,001-$100,000

1.94%

$101,000-$150,000

1%

More than $150,000

1.16%

What type of health insurance do you have?

Employer-provided

37.65%

Medicare or Medicaid

45.88%

Self-purchased through an exchange

11.76%

None

4.71%

What is the primary source of your medical debt?

Diagnostic tests

23.77%

Hospitalization

18.33%

Emergency room

18.56%

Outpatient services

15.16%

Doctor visits

13.11%

Dental care

6.15%

Prescription drugs

4.10%

Nursing home/long-term care

0.82%

How did your insurance company respond to your medical bills?

Told me I received out-of-network care

14.54%

Denied my claim

13.22%

Other – N/A

72.24%

Have you tried negotiating to lower the cost of your bills?

Yes, I tried to negotiate on my own

35.32%

Yes, I used a medical bills advocate

4.25%

No

60.40%

Were you successful in this negotiation?

Yes

34.04%

No

65.96%

Are you currently on a payment plan?

Yes

34.63%

No

65.37%

For full 2020 survey results, click here

Do you have outstanding medical bills or medical debt?

Yes

45.87%

No

54.13%

Have your medical bills been sent to collections?

Yes

56.16%

No

30.78%

Unsure

13.06%

How much do you owe in medical debt?

Less than $500

13.77%

$501-$1,000

18.55%

$1,001-$5,000

31.93%

$5,001-$10,000

14.91%

$10,001-$50,000

15.30%

$50,001-$100,000

3.06%

$101,000-$150,000

0.96%

More than $150,000

1.53%

What type of health insurance do you have?

Employer-provided

43.13%

Medicare or Medicaid

36.17%

Self-purchased through an exchange

8.90%

None

11.80%

What is the primary source of your medical debt?

Diagnostic tests

21.68%

Hospitalization

24.80%

Emergency room

18.95%

Outpatient services

10.94%

Doctor visits

14.84%

Dental care

4.30%

Prescription drugs

3.71%

Nursing home/long-term care

0.78%

How did your insurance company respond to your medical bills?

Told me I received out-of-network care

55.80%

Denied my claim

44.20%

Have you tried negotiating to lower the cost of your bills?

Yes, I tried to negotiate on my own

34.55%

Yes, I used a medical bills advocate

4.94%

No

60.52%

Were you successful in this negotiation?

Yes

27.47%

No

72.53%

Methodology: Debt.com surveyed 682 people and asked 18 questions related to their medical debt. People responded from all 50 states and Washington, DC and were aged 18 and above. Responses were collected through SurveyMonkey. The survey was conducted on April 10, 2025.

Getting out of debt isn’t one-size-fits-all. There are dozens of private and government programs, and each one works best under certain circumstances. See how those options might affect you.

Step 1

How much do you owe?

$25,000

Pros and Cons

Let Debt.com Help You Choose the Best Plan

Talk to a debt relief specialist to weigh your options.

Minimum payment calculation assumes an APR of 24% on your credit card debt and each monthly payment is 3% of total amount.

Debt Consolidation

Assumes a loan APR of 16.5% over a 5- year term.

Debt Management Program

Average Interest Rate in a DMP is 8%. Actual interest rates will vary by consumer and creditor.

A DMP might be able to reduce your interest rates and late fees allowing you to pay off your credit card debt quicker (since more payments are applied to your principal balances, saving you lots of money in the long run). To complete the program, you must make on-time payments each month. Late or missed payments may cause your program to be canceled and in that event, this estimate would not apply to you.

Debt Settlement

Rates and terms vary by consumer and creditor. Debt settlement may negatively impact your credit score.

*Debt settlement fees vary by program and state.

Our Site uses cookies and pixels for compliance, user interactions recording, and relevant marketing services. 3rd-party cookies and pixels may share information with 3rd-party associates. Essential cookies cannot be rejected. By taking No Action, clicking the "[X]" or "ACCEPT ESSENTIAL COOKIES" you are accepting Essential Cookies and Pixels. To accept all cookies and pixels click "ACCEPT ALL COOKIES". By using the Site, you agree you read and accepted our Privacy Policy, Terms of Use, and Arbitration Agreements.