Debt.com’s writers are journalists, personal finance experts, and certified credit counselors. Their advice about money – how to make it, how to save it, and how to spend it – is based on, collectively, a century of personal finance experience. They’ve been featured in media outlets ranging from The New York Times to USA Today, from Forbes to FOX News, and from MSN to CBS.

66% of Americans Say Tariff-Driven Inflation Is Taking a Mental Toll

Debt.com survey reveals a strong link between financial pressures and emotional health during Mental Health Awareness Month

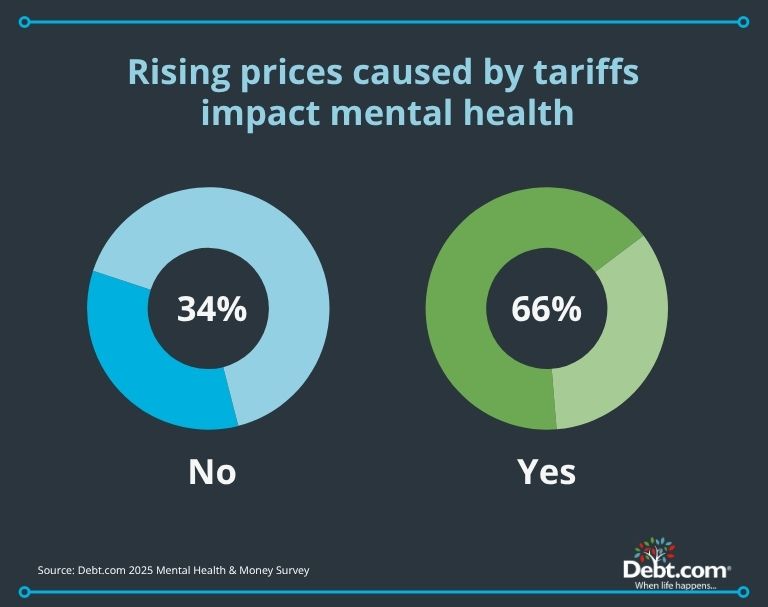

Tariffs are doing more than driving up the cost of everyday essentials — they’re also weighing heavily on the minds of American consumers. According to a new national survey from Debt.com, 66% of respondents say tariff-related price increases are negatively affecting their mental health.

The emotional fallout is real — and growing. Among those impacted by rising prices caused by tariffs on imports from China and other countries, the emotional strain is significant:

75% say they feel stressed

74% report feeling anxious

38% feel sad

33% describe feeling hopeless

23% say it’s affecting their focus at work

17% are losing sleep

7% report they’re unable to eat

“Inflation is more than an economic issue — it’s a mental health issue,” says Howard Dvorkin, CPA, chairman of Debt.com. “When prices go up and paychecks don’t, Americans feel the pressure not just in their wallets, but in their emotional well-being.”

Each May, in recognition of Mental Health Awareness Month, Debt.com surveys 1,000 Americans to understand the emotional impact of financial stress. While tariffs and inflation topped the list this year, they’re just one part of a broader financial mental health crisis — one that’s affecting everything from sleep to workplace performance.

Since President Trump’s inauguration, his administration has yo-yoed tariffs on countries around the globe. The major one was “reciprocal tariffs” on China that hit as high as 145%, which has since been lowered to 10% on a 90-day pause, as of May 12. The price increases have led to an increase in financial stress.

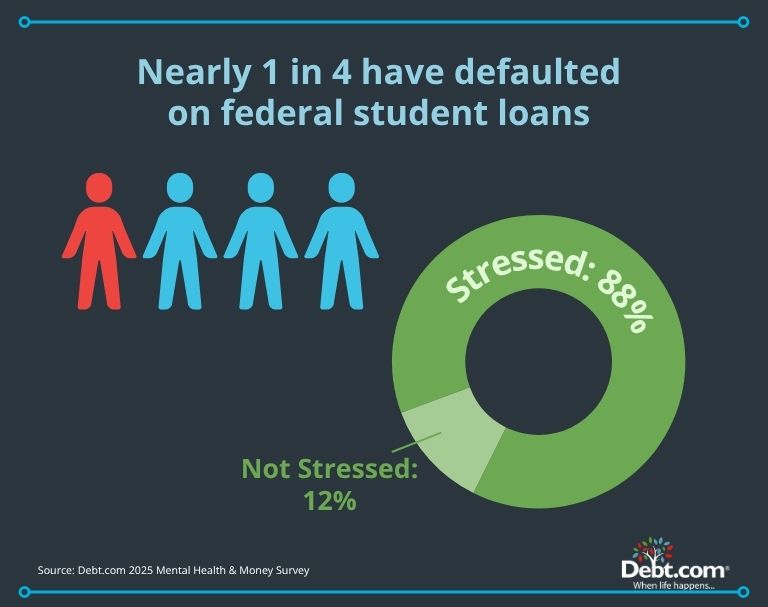

On May 5, the U.S. Department of Education announced it would begin collection on defaulted student loans after a five-year pause. More than 5 million student loan borrowers were in default – 1 in 4 of whom Debt.com surveyed.

Almost 9 in 10 respondents report feeling “stressed about the possibility of the federal government garnishing wages, tax refund, or benefits.

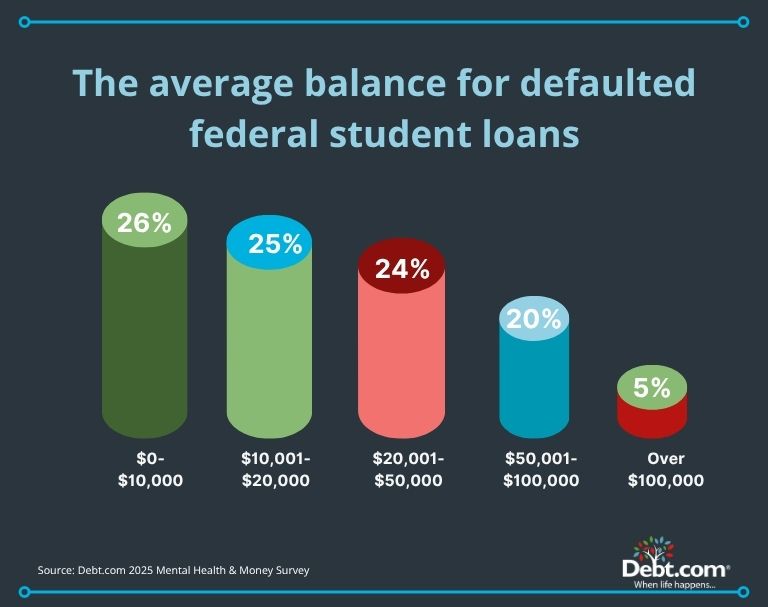

Of those with student loans in default, 35% owe $30,000 or more, and one in four owe at least $50,000 to $75,000.

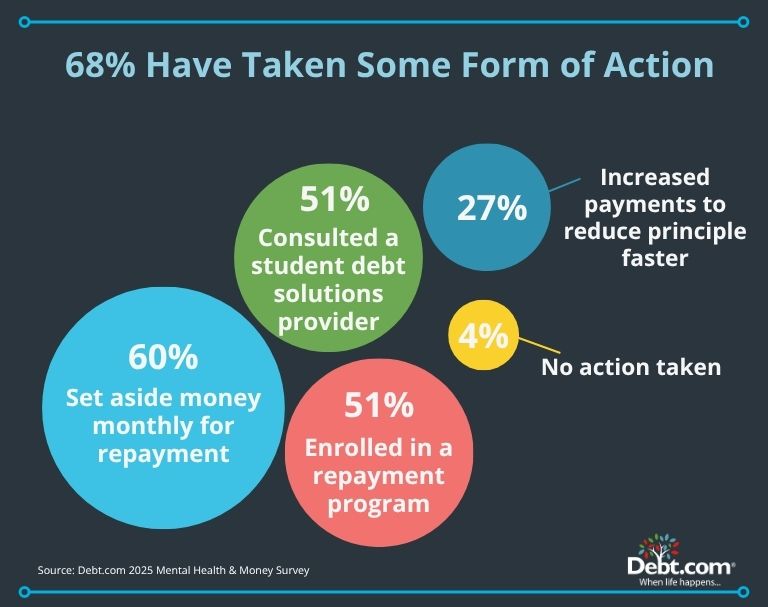

Nearly 1 in 3 borrowers with defaulted federal student loans haven’t taken any steps to prepare for collections resuming.

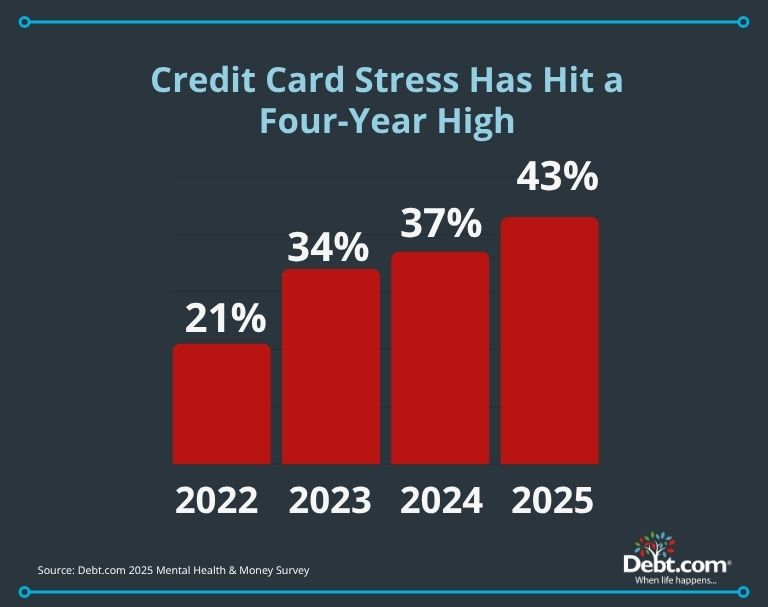

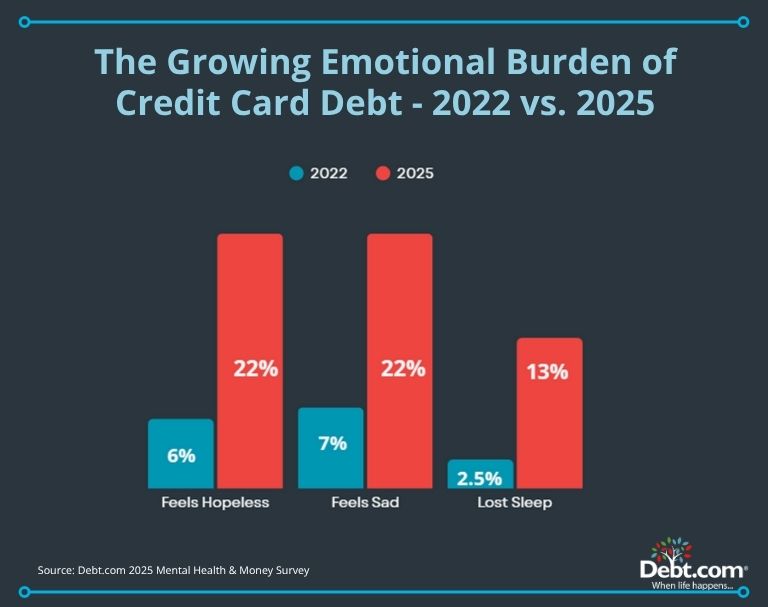

Stress linked to credit card use has surged by 22 percentage points over the past four years – reaching its highest level since tracking began. In 2022, just 21% of respondents said they felt stress from using their credit cards. That number has steadily increased each year.

This sharp rise reflects the ongoing pressure of inflation, rising interest rates, and stagnant wages, which are forcing more Americans to rely on credit cards to cover everyday expenses.

“Credit cards were once used for emergencies or rewards,” says Howard Dvorkin, CPA and chairman of Debt.com. “Now, they’ve become a lifeline — and that’s creating serious emotional and financial strain.”

Click here for full survey results

Do rising prices caused by tariffs on goods from China and other countries negatively impact your mental health?

Yes

66.04%

No

33.96%

If yes, how would you describe how you feel?

Stressed

74.85%

Anxious

73.93%

Hopeless

33.38%

Sad

37.50%

I’m losing sleep

17.07%

I can’t eat

6.86%

It’s on my mind while at work

23.17%

N/A

1.07%

Do you currently have defaulted federal student loans?

Yes

23.17%

No

76.83%

How much do you currently owe in student loan debt?

$0-$5,000

12.55%

$5,001-$10,000

12.97%

$10,001-$15,000

10.46%

$15,001-$20,000

15.06%

$20,001-$30,000

14.23%

$30,001-$50,000

9.62%

$50,001-$75,000

10.46%

$75,001-$100,000

10.04%

Over $100,000

4.60%

Are you stressed about the possibility of the federal government garnishing your wages, tax refunds, or benefits?

Yes

88.19%

No

11.81%

Have you taken action in anticipation of the Trump administration’s announcement about student loan collections resuming?

Yes

68.35%

No

31.65%

What precautions have you taken in response to the announcement?

I’ve started setting aside money monthly for repayment

60.49%

I’ve consulted a student debt solutions provider

51.23%

I’ve enrolled in Education Department repayment programs

50.62%

I plan to increase my payments to reduce the principal faster

27.16%

I haven’t taken action; I’m waiting to see what happens

3.70%

Do you believe the convenience of credit cards can negatively impact mental health?

Yes

71.39%

No

28.61%

How do you feel after using your credit card(s)?

Content

50.82%

Stressed

42.65%

Guilty

30.92%

Sad

10.10%

Embarrassed

7.24%

Are you more or less likely to take on additional debt when feeling stressed?

Very likely

13.94%

Likely

20.35%

Neither likely nor unlikely

31.94%

Unlikely

15.67%

Very unlikely

18.11%

How do you feel when reviewing your credit card bills?

Stressed

49.24%

Sad

22.29%

Hopeless

21.78%

I lose sleep

13.37%

I lose my appetite

6.79%

I feel lower self-esteem

14.69%

None of the above

34.65%

How does credit card debt affect your social life?

My significant other and I argue over my credit card spending

17.74%

I avoid dating

13.23%

I hide my credit card spending from my significant other

15.59%

I avoid going out with my friends or family

23.18%

I avoid talking about money or future plans

24.21%

My credit card debt doesn’t affect my social life

46.77%

Do you avoid looking at your credit card bill because it is too painful?

Yes

38.32%

No

61.68%

Have you missed a credit card payment because you couldn’t bring yourself to look at the balance?

Yes

25.33%

No

74.67%

Have you ever applied for a new credit card because you were sad or stressed?

Yes

25.79%

No

74.21%

How often do you impulsively buy items or services with your credit card that you regret later?

Weekly

12.99%

Monthly

18.68%

A few times a year

40.30%

Never

28.02%

How much debt have you incurred from impulsive shopping due to stress or feeling down?

$1-$1,000

58.63%

$1,001-$5,000

17.58%

$5,001-$10,000

10.34%

$10,001-$15,000

6.83%

$15,001-$20,000

3.62%

Over $20,000

3.00%

Click here for full 2024 survey results

Do you think the convenience of credit cards can negatively impact mental health?

Yes

76.14%

No

23.86

How do you feel after using your credit card(s)?

Content

39.87%

Stressed

37.45%

Guilty

17.20%

Sad

2.79%

Embarrassed

2.40%

Are you more or less likely to take on more debt when feeling stressed?

Very likely

28.53%

Likely

18.25%

Somewhat likely

16.81%

Neither likely nor unlikely

12.97%

Somewhat unlikely

5.96%

Unlikely

9.13%

Very unlikely

8.36%

How do you feel while reviewing your credit card bills?

Stressed

50.91%

Sad

8.36%

Hopeless

9.51%

Loss of sleep

4.03%

Loss of appetite

2.69%

Lower self-esteem

2.79%

None of the above

21.71%

How does credit card debt affect you socially?

My significant other and I argue over my credit card spending

25.55%

I avoid dating

5.96%

I hide my credit card spending from my significant other

10.47%

I avoid going out with my friends or family

10.47%

I avoid talking about money or my future plans

14.70%

My credit card debt doesn’t affect my social life

32.85%

Do you avoid looking at your credit card bill because it’s too painful to do so?

Yes

58.21%

No

41.88%

Have you missed a credit card payment because you couldn’t bring yourself to look at the balance?

Yes

44.96%

No

55.04%

Have you ever applied for new credit cards because you were sad or stressed?

Yes

46.30%

No

53.70%

How often do you impulsively buy items or services with your credit card that you regret later?

Once a week

25.94%

Monthly

24.78%

Few times a year

31.80%

Never

17.48%

How much debt have you incurred from impulsive shopping because you were feeling down or stressed out?

$1-$1,000

40.54%

$1,000-$5,000

22.86%

$5,000-$10,000

9.51%

$10,000-$15,000

11.72%

$15,000-$20,000

9.70%

More than $20,000

5.67%

Click here for full 2023 survey results

How do you feel after using your credit card(s)?

Content

44.55%

Stressed

33.93%

Guilty

15.73%

Sad

2.94%

Embarrassed

2.84%

How do your credit card bills affect you?

Makes me feel stressed

42.65%

Makes me feel sad

6.92%

Makes me feel hopeless

8.15%

Loss of sleep

2.75%

Loss of appetite

0.95%

Lower self-esteem

2.56%

None of the above

36.02%

How does credit card debt affect you socially?

My significant other and I argue over my credit card spending

11.28%

I avoid dating

4.74%

I hide my credit card spending from my significant other

11.28%

I avoid going out with friends or family

9.57%

I avoid talking about money or my future plans

11.47%

My credit card debt doesn’t affect my social life

51.66%

Do you avoid looking at your credit card bill because it is too painful to do so?

Yes

37.44%

No

62.56%

Have you missed a credit card payment because you just couldn’t bring yourself to look at the balances?

Yes

22.18%

No

77.82%

Have you ever applied for new credit cards because you were sad or stressed?

Yes

25.59%

No

74.41%

How often do you impulsively buy items or services with your credit card that you later regret?

Once weekly

11.85%

Monthly

19.35%

Few times a year

37.54%

Never

31.09%

How much debt have you incurred from impulse shopping because you were feeling fown or stressed out?

$1-$1,000

63.70%

$1,001-$5,000

16.11%

$5,001-$10,000

9.95%

$10,001-$15,000

4.55%

$15,001-$20,000

2.37%

More than $20,000

3.32%

Do you think the convenience of credit cards can negatively impact mental health?

Yes

78.39%

No

21.61%

Click here for full 2022 survey results

How do you feel after using your credit card(s)?

Content

53.20%

Stressed

21.39%

Guilty

19.01%

Sad

5.64%

Embarrassed

0.76%

How do your credit card bills affect you?

Makes me feel stressed

38.59%

Makes me feel sad

6.78%

Makes me feel hopeless

6.40%

Loss of sleep

2.58%

Loss of appetite

0.86%

Lower self-esteem

2.01%

None of the above

42.79%

How does credit card debt affect you socially?

My significant other and I argue over my credit card spending

3.15%

I avoid dating

5.16%

I hide my credit card spending from my significant other

5.83%

I avoid going out with friends or family

10.32%

I avoid talking about money or my future plans

19.01%

My credit card debt doesn’t affect my social life

56.54%

Do you avoid looking at your credit card bill because it is too painful to do so?

Yes

32.38%

No

67.62%

Have you missed a credit card payment because you just couldn’t bring yourself to look at the balance?

Yes

46.31%

No

53.69%

Have you ever applied for new credit cards because you were sad or stressed?

Yes

19.10%

No

80.90%

How often do you impulsively buy items or services with your credit card that you later regret?

Once weekly

8.40%

Monthly

18.15%

Few times yearly

39.73%

Never

33.72%

How much debt have you incurred from impulse shopping because you were feeling down or stressed out?

$1-$1,000

51.44%

$1,001-$5,000

24.93%

$5,001-$10,000

13.26%

$10,001-$15,000

4.18%

$15,001-$20,000

2.88%

More than $20,000

3.31%

Do you think the convenience of credit cards can negatively impact mental health?

Yes

74.40%

No

25.60%

Methodology: Debt.com surveyed more than 1,000 Americans and asked 17 questions about how their finances impact mental health. People responded from all 50 states and Washington, DC and were aged 18 and above. Responses were collected through SurveyMonkey. Percentages were rounded up to the nearest whole number and might not total 100 percent. The survey was conducted on May 12, 2025.

Getting out of debt isn’t one-size-fits-all. There are dozens of private and government programs, and each one works best under certain circumstances. See how those options might affect you.

Step 1

How much do you owe?

$25,000

Pros and Cons

Let Debt.com Help You Choose the Best Plan

Talk to a debt relief specialist to weigh your options.

Minimum payment calculation assumes an APR of 24% on your credit card debt and each monthly payment is 3% of total amount.

Debt Consolidation

Assumes a loan APR of 16.5% over a 5- year term.

Debt Management Program

Average Interest Rate in a DMP is 8%. Actual interest rates will vary by consumer and creditor.

A DMP might be able to reduce your interest rates and late fees allowing you to pay off your credit card debt quicker (since more payments are applied to your principal balances, saving you lots of money in the long run). To complete the program, you must make on-time payments each month. Late or missed payments may cause your program to be canceled and in that event, this estimate would not apply to you.

Debt Settlement

Rates and terms vary by consumer and creditor. Debt settlement may negatively impact your credit score.

*Debt settlement fees vary by program and state.

Our Site uses cookies and pixels for compliance, user interactions recording, and relevant marketing services. 3rd-party cookies and pixels may share information with 3rd-party associates. Essential cookies cannot be rejected. By taking No Action, clicking the "[X]" or "ACCEPT ESSENTIAL COOKIES" you are accepting Essential Cookies and Pixels. To accept all cookies and pixels click "ACCEPT ALL COOKIES". By using the Site, you agree you read and accepted our Privacy Policy, Terms of Use, and Arbitration Agreements.