Debt.com’s writers are journalists, personal finance experts, and certified credit counselors. Their advice about money – how to make it, how to save it, and how to spend it – is based on, collectively, a century of personal finance experience. They’ve been featured in media outlets ranging from The New York Times to USA Today, from Forbes to FOX News, and from MSN to CBS.

Summer Vacation Spending Survey: 8 in 10 Travelers Will Use Credit Cards This Summer

And many have already gone into debt for previous trips.

When Americans travel this summer, almost all of them will put it on their credit cards – and more than a quarter (30%) of them will spend at least $5,000.

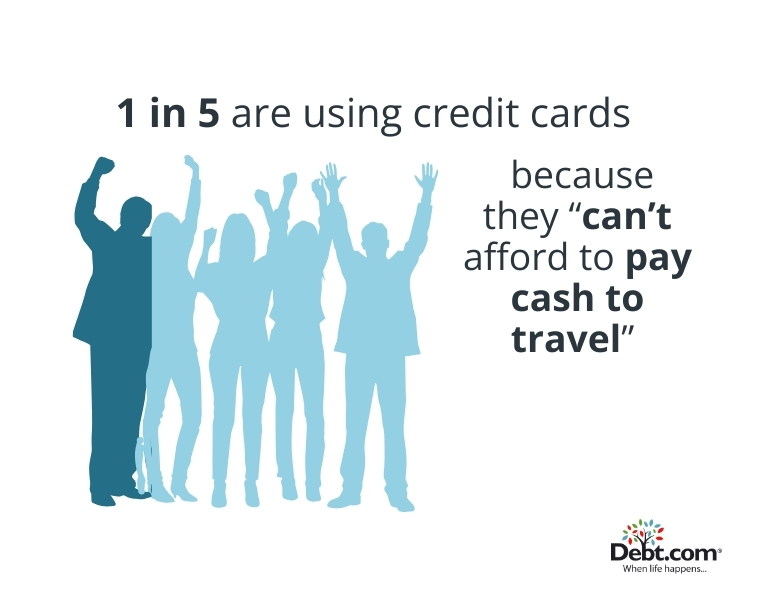

A new Debt.com survey of 500 Americans shows 83% will pay for their trip using credit cards. Why credit cards? More than half (56%) say they’ll “earn cashback and rewards,” while 19% “can’t afford to pay cash, but still feel the need to get away this summer.”

For many, this is a repeat habit.

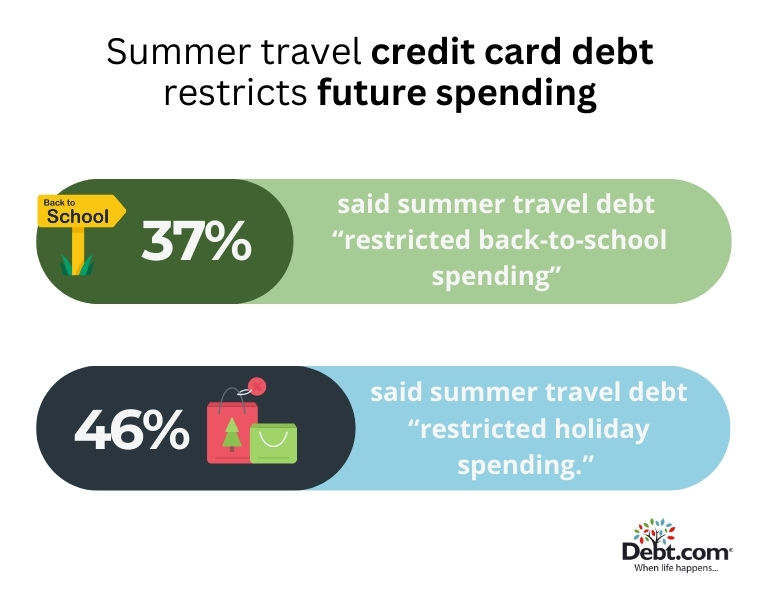

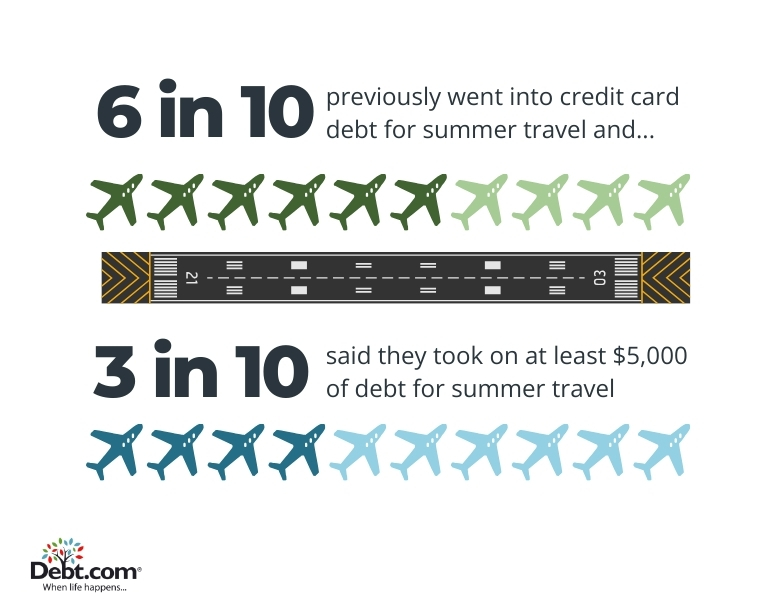

Just under 3 in 5 (59%) “have gone into debt for summer travel in the past.” Just over 1 in 3 (38%) say that debt restricted their back-to-school spending – and 46% had to cut back spending during the winter holidays.

Key findings

Nearly 3 in 5 summer travelers will use credit cards to pay for a vacation. Of those respondents, 3 in 10 (30%) plan to charge at least $5,000 for their vacation – with 7% planning to charge $15,000 or more.

Just under 1 in 5 (19%) said they’re using credit cards because they “can’t afford to pay cash to travel.” That includes 25% of Gen X, 18% of Millennials, 14% of Baby Boomers, and 9% of Gen Z.

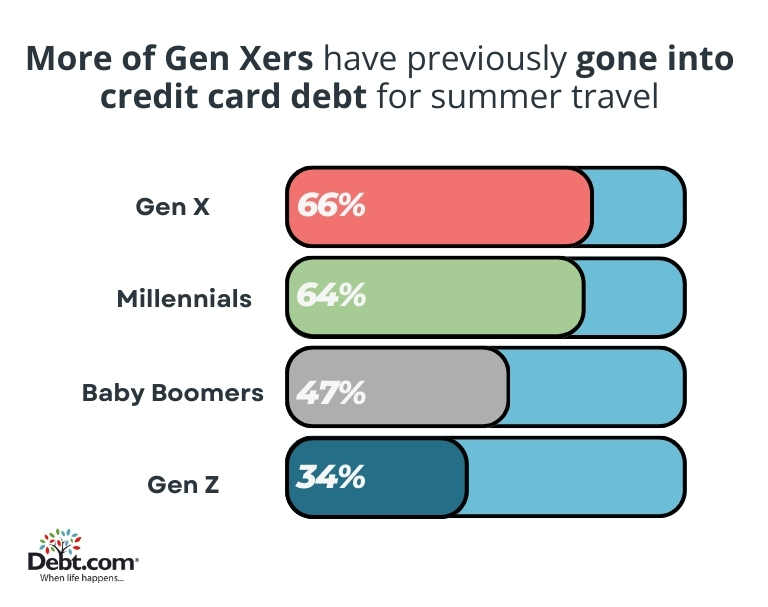

Just under 3 in 5 (59%) of respondents have previously gone into credit card debt for summer travel. That includes 66% of Gen X, 64% of Millennials, 47% of Baby Boomers, and 34% of Gen Z.

More than 1 in 4 (27%) said they previously took on at least $5,000 for summer travel. It took 1 in 4 of them six months to a year to pay back the debt. Meanwhile, it took 15% more than a year.

Over 1 in 3 (37%) of respondents said their summer travel debt later “restricted their back-to-school spending. That includes just under half (49%) of Gen X, 42% of Millennials, 30% of Gen Z, and 11% of Baby Boomers.

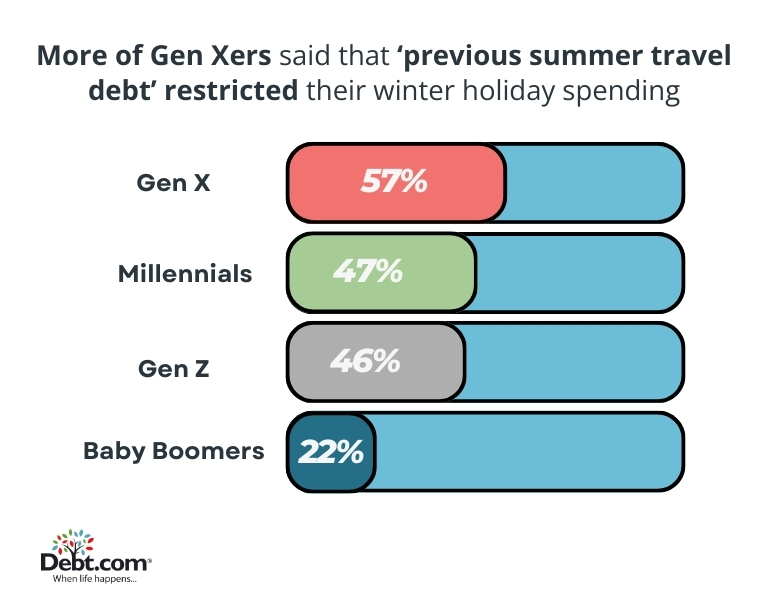

More than 4 in 10 (46%) said their summer travel debt “restricted their holiday spending.” That includes More than half (57%) of Gen X, 47% of Millennials, 46% of Gen Z, and 22% of Baby Boomers.

How many people finance vacations?

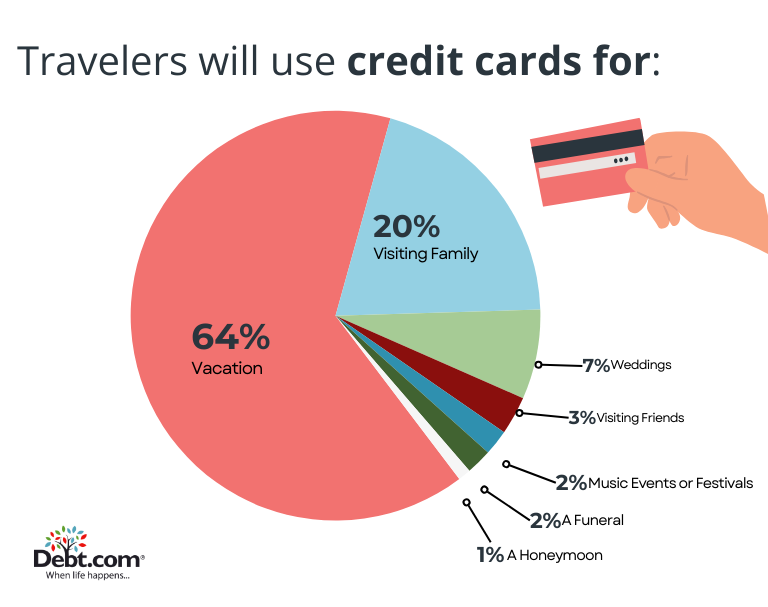

What will summer travelers use credit cards to pay for?

How summer travelers pay for vacation when they don’t have cash

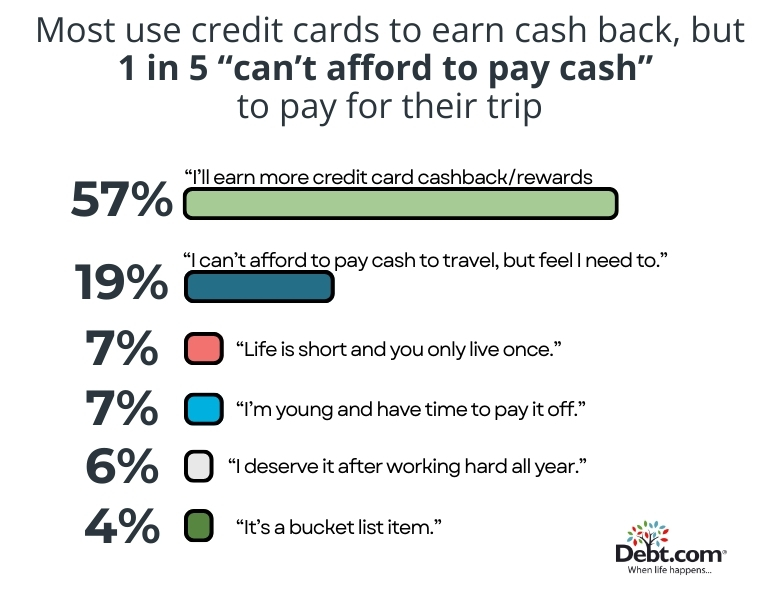

Why will summer travelers use credit cards for vacation?

Which generation has the most credit card debt from travel?

How summer travel credit card debt restricts future spending

How many Americans have summer travel credit card debt

Full survey results

Do you plan on using credit cards for summer travel?

Yes

82%

No

18%

How much do you plan on charging on your credit cards?

$0-$1,500

30%

$1,500-$2,500

21%

$2,500-$5,000

20%

$5,000-$7,000

11%

$7,000-$10,000

9%

$10,000-$15,000

4%

$15,000+

5%

What type of travel will you use credit cards for?

Vacation

64%

Wedding

8%

Visit family

20%

Funeral

2%

Honeymoon

1%

Visit friends

3%

Music event or festival

2%

Why will you use credit cards and possibly go into debt to travel this summer?

I can’t afford to pay cash to travel, but feel I need to

19%

I’ll earn more credit card cashback/rewards and I’ll just pay it back later in the year

57%

I’m young and have time to pay it off

7%

It’s a bucket list item

4%

I deserve it after working hard all year

6%

Life is short and you only live once

7%

How long do you think it will take you to pay the credit card debt back?

1-3 months

44%

3-6 months

20%

6-12 months

21%

1-2 years

10%

3-5 years

4%

Never, I don’t believe I can pay it back.

1%

Have you ever gone into credit card debt for summer travel in the past?

Yes

59%

No

41%

How much credit card debt did you take on for that summer trip?

$0-$1,500

39%

$1,500-$2,500

18%

$2,500-$5,000

15%

$5,000-$7,000

12%

$7,000-$10,000

5%

$10,000-$15,000

4%

$15,000+

5%

What type of summer travel caused you to go into debt?

Vacation

62%

Wedding

8%

Visit family

17%

Funeral

4%

Honeymoon

3%

Visit friends

4%

Music event or festival

2%

Why did you take on credit card debt for that summer trip?

I couldn’t afford it, but felt I needed to

19%

After years in lockdown from the pandemic, it was my “revenge travel”

17%

I thought I’d earn more cashback and rewards on my credit card and pay it back

34%

I was young and foolish with my money

7%

It was a bucket list item

5%

I deserved it after working hard all year

9%

Life is short and you only live once

10%

How long did it take you to pay the debt back?

1-3 months

40%

3-6 months

21%

6-12 months

23%

1-2 years

10%

3-5 years

4%

I haven’t fully paid it back and still owe money on the debt

2%

Did summer travel debt later restrict your back-to-school shopping?

Yes

38%

No

38%

Not applicable

24%

Did summer travel debt later restrict your holiday spending?

Yes

46%

No

54%

Methodology: Debt.com surveyed more than 500 Americans and asked 12 questions about their summer travel plans. People responded from all 50 states and Washington, DC and were aged 18 and above. Responses were collected through SurveyMonkey. Percentages were rounded up to the nearest whole number and might not total 100 percent. The survey was conducted on May 22, 2024.

Getting out of debt isn’t one-size-fits-all. There are dozens of private and government programs, and each one works best under certain circumstances. See how those options might affect you.

Step 1

How much do you owe?

$25,000

Pros and Cons

Let Debt.com Help You Choose the Best Plan

Talk to a debt relief specialist to weigh your options.

Minimum payment calculation assumes an APR of 24% on your credit card debt and each monthly payment is 3% of total amount.

Debt Consolidation

Assumes a loan APR of 16.5% over a 5- year term.

Debt Management Program

Average Interest Rate in a DMP is 8%. Actual interest rates will vary by consumer and creditor.

A DMP might be able to reduce your interest rates and late fees allowing you to pay off your credit card debt quicker (since more payments are applied to your principal balances, saving you lots of money in the long run). To complete the program, you must make on-time payments each month. Late or missed payments may cause your program to be canceled and in that event, this estimate would not apply to you.

Debt Settlement

Rates and terms vary by consumer and creditor. Debt settlement may negatively impact your credit score.

*Debt settlement fees vary by program and state.

Our Site uses cookies and pixels for compliance, user interactions recording, and relevant marketing services. 3rd-party cookies and pixels may share information with 3rd-party associates. Essential cookies cannot be rejected. By taking No Action, clicking the "[X]" or "ACCEPT ESSENTIAL COOKIES" you are accepting Essential Cookies and Pixels. To accept all cookies and pixels click "ACCEPT ALL COOKIES". By using the Site, you agree you read and accepted our Privacy Policy, Terms of Use, and Arbitration Agreements.