People often say there are only two certainties in life: Death and taxes. And though death usually signifies the end of earthly connections, debt has a way of lingering. That’s why ensuring your loved ones are financially secure after you’re gone is important. The last thing you want is for debt collectors to harass your grieving family members. So, if you have debt, knowing exactly what will happen to your debts when you die would be wise.

Ignoring what happens to your debt when you die causes more stress. The truth is your loved ones likely won’t inherit most of your unsecured debts from credit cards or payday loans.

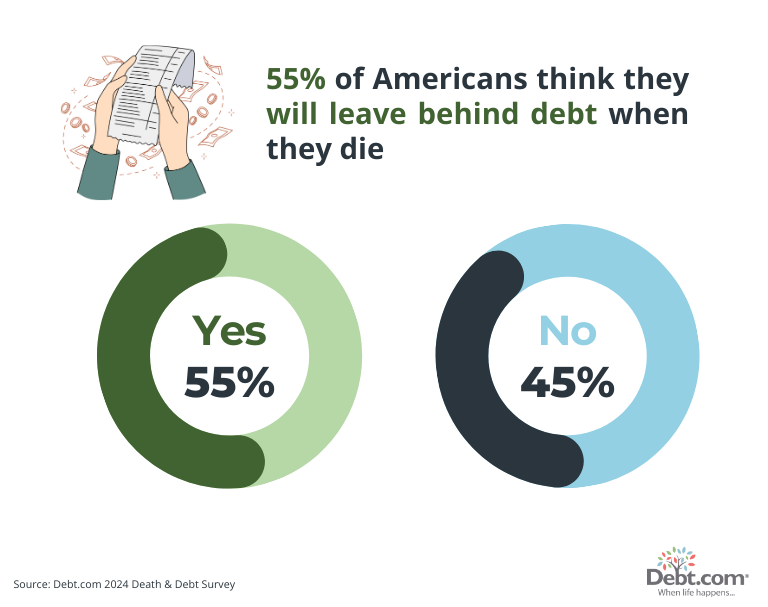

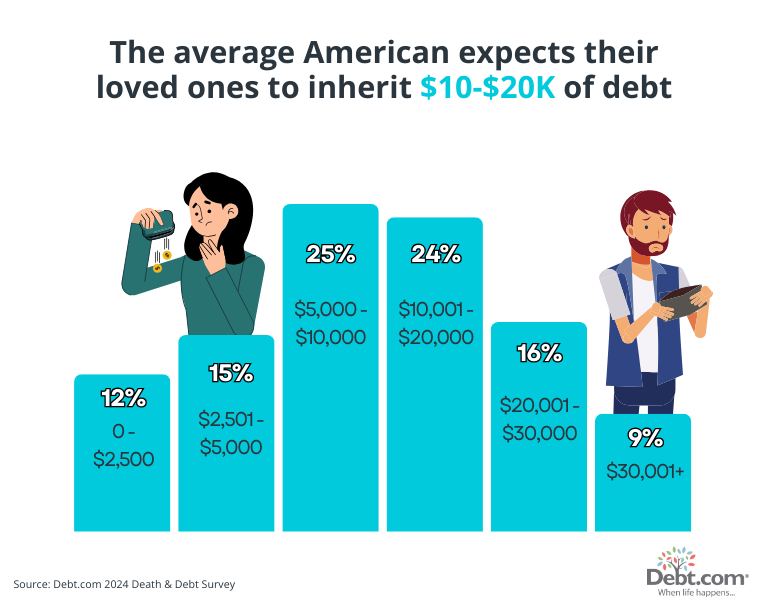

In fact, Debt.com polled 1,000 Americans for its annual Death and Debt survey. More than half expect to pass on debt to family members when they die, and one in four thinks between $10,000 and $20,000.

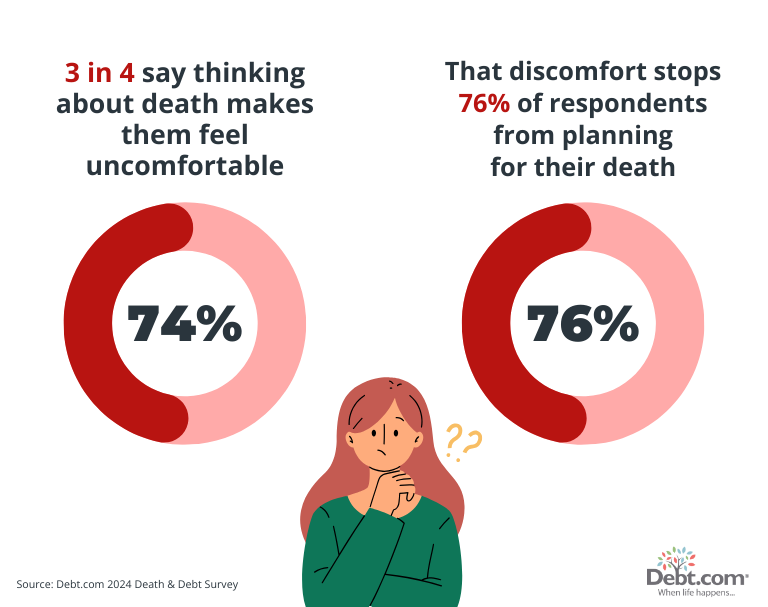

“Most Americans don’t know which debts they inherit and which they don’t,” says Debt.com president Don Silvestri. “The topic isn’t confusing; it’s just uncomfortable. So many of us avoid it entirely.”

Read on if you’re like the 40% of Debt.com’s survey respondents who don’t know what happens to their debt when they die.

Table of Contents

What happens to debt after death?

To ensure your assets get to their rightful heir, you’re going to need to plan how you’ll do that — and make a plan to take care of all your debt once you’re gone. It’s called estate planning and will involve you writing out a will, which is a basic document explaining who gets what and who’s in charge of your estate after your death.

In your will, you appoint someone as your representative, commonly referred to as your executor. They will be responsible for tracking down your creditors through a legal process called probate and making sure they receive payment from your estate. Your heirs will benefit from your will once the debts are taken care of.

There are situations where heirs may not receive anything. This is because the deceased’s debts outweigh their assets. In that case, creditors may not receive anything, either. That’s because creditors can make legal claims against the estate but can’t go after your inheritors. Once the estate’s money is gone, there’s nothing left to pay them. But the good news is that they can’t go after your loved ones to make up any difference.

What happens to mortgage debt when you die?

When you die, your debts can deplete assets you may have hoped to pass on to your heirs. Your estate can only leave them what is left after debts are deducted from the overall estate.

Mortgages are considered secured debts. A mortgage is a large loan to borrow, so the lender needs protection in case the borrower defaults on their loan. If the borrower doesn’t fulfill their obligations, the lender uses the borrower’s house as collateral by foreclosing on the home and selling it for payment.

When you die, your estate takes responsibility for paying back your remaining debts. Because mortgages are secured debts, those lenders will get first dibs for creditors to receive payment, compared to let’s say a credit card, which is unsecured.

If you want to leave your home to someone, make it clear in your will. If your mortgage isn’t paid in full, the heir will take that responsibility as long as they can afford to pay for it.

What happens to my mortgage if my spouse dies before me?

It’s not uncommon for one spouse in a marriage to pass away before the other. And odds are you owned your home together. According to the National Association of Realtors’ 2018 Buyer and Sellers Generational Trends report, 65% of recent homebuyers are married. That means most deceased homeowners are likely married at their time of death.

When one of the spouses dies with an outstanding mortgage, the survivor fully takes over the mortgage. But your spouse may have the only name on the mortgage. If so, then they need to leave the home to you in their will. If they don’t, the rest of the family could find themselves in a pinch.

Whether you are a joint homeowner — or are set to inherit the home — you will be responsible for your spouse’s mortgage debt after they die.

What if I die with a mortgage but never married?

Just because you never married, it doesn’t mean you can’t leave your home to someone important to you. Make it clear in your will if there is a specific beneficiary you’d like to see take ownership of your home.

If not, your estate will pay out the debt that is left. If there aren’t enough funds in your estate to cover your mortgage debt, your lender is out of luck. They can’t squeeze blood from a turnip.

When that beneficiary takes ownership of your home, they also take ownership of the mortgage. Following your death, they will contact the lender, notifying them that they will take over the mortgage.

There is a chance they may not qualify for a mortgage on their own. But if they’re able to keep up with your original mortgage payment, they’re allowed to keep the home. Once the home is in their name, they can do as they wish with it.

They can refinance your home (usually for better interest rates). Or, if they can’t afford the mortgage and your estate is unable to pay off the balance, they can leave the house for the bank to foreclose on it.

What happens to auto loans after death?

Here is another example of a secured debt. The lender can repossess the vehicle if the borrower doesn’t keep up with their monthly bills. If your spouse purchased a new vehicle shortly before passing on, odds are they left behind an auto loan.

There is one definite way you will end up with your deceased spouse’s auto loan tab. And that way comes down to one question: where do you live?

There are nine states in the U.S. where laws mandate that married couples split half of their assets and half of all debts. They’re called community property states. And if your spouse financed a $20,000 vehicle, you are responsible for half of the car’s loan balance. This only happens if the loan was taken out during your marriage. Those states are the following…

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

…If they die owing a balance of $18,000, you’re responsible for $9,000 of that debt.

In any state, regardless of where you live, if you cosigned on your deceased spouse’s auto loan, then you are responsible for paying it back in full.

What happens to credit card debt when you die?

If you were the only account holder on the card, the debt is yours alone. Only the estate can be held liable to pay off the remaining balance. Once the estate is closed, credit card debts can’t pass to your heirs.

The estate’s executor is responsible for notifying all credit card companies that the account holder has passed away. This closes the accounts to avoid additional interest charges. The executor is also responsible for officially closing the account.

To do that, the executor will need to send a registered, certified letter in writing. On top of that, the credit card company will usually request a death certificate. This is why if you’re someone’s executor, make sure to get as many copies of the death certificate as possible. You’re going to need them.

The executor must notify the Big Three credit bureaus of the account holder’s death.

Big Three credit bureaus:

- Equifax

- Experian

- Transunion

This is important to ensure the credit report is flagged as “deceased.” Fraudulent credit cards cannot be opened in the deceased person’s name.

Will I be responsible for my spouse’s credit card debt after their death?

No, for the most part. Only the estate of the deceased person takes responsibility for the debt. You could be on the hook in a few situations, though.

One instance where you’re always going to be responsible for paying your spouse’s debt is when you are a joint account holder or cosigner on the credit card. Another is when they have outstanding credit card balances and live in a community property state.

There are nine of them in this country. If you live in one of these states, both partners in the marriage take 50/50 ownership of all assets and all debts. So, if your spouse dies, you inherit half of their debts along with half of their assets.

Who’s responsible for my spouse’s credit card debt after death?

There is a possibility that someone else, such as a joint account holder or cosigner, will take responsibility for your credit card debt after you die.

A joint account holder will be responsible for your leftover debt from that credit card, but this same rule doesn’t apply to an authorized user. An authorized user and a joint account holder can charge the account. However, an authorized user doesn’t build a credit history for using an account. The upside is that they aren’t responsible for the debt either.

Authorized users vs. joint account holders

The biggest difference between an authorized user and a joint account holder is who is legally obligated for the credit card balance — even after death.

The authorized user accepts zero legal obligation to the debt. The authorized user can walk away from the debt if the credit card holder passes while the two share an account. Just ensure you don’t try to make new charges to the account, especially after the executor informs the credit card company that the account holder has passed away.

This isn’t the same for a joint account holder or a co-signer.

A joint account holder is jointly responsible for the debt. With cosigners, the cosigner accepts as much responsibility as the primary holder. In that sense, the credit card issuer can pursue the cosigner the same way they would the primary.

If the primary account holder’s death leaves an active balance, the joint account holder and cosigner are responsible for paying it.

If you’re the executor of the deceased’s estate, you must ensure any authorized account users are notified of the primary account holder’s death. And that they can no longer make charges with the credit card.

Using a deceased person’s credit card — even if authorized to do so — is considered fraud. This doesn’t apply to a joint account holder; no changes will be made in how they use the account.

Talk to a debt relief specialist to find the best way to pay off credit card debt.

What happens to student loan debt when you die?

Determining whether your student loan debt will get passed on to your spouse or other family members comes down to what type of loans you have.

Student loans are lent out uniquely. Some are administered by the federal government through the Department of Education, while others are from private banks and financial institutions.

The biggest difference between these two types is the interest rates. Federal loans tend to have lower interest rates, while private lenders set the interest they charge.

Am I responsible for my spouse’s federal student loans after their death?

Student loans obtained through FAFSA from the Department of Education do not need to be paid back after a borrower’s death.

Just like credit card issuers, student loan servicers need documentation with a death certificate to prove the borrower’s death. The Federal Student Aid website does outline that acceptable documentation includes:

- An original death certificate,

- a certified copy of the death certificate,

- or an accurate and complete photocopy of one of those documents.

If a borrower dies, their federal student loan debt dies with them.

The Department of Education cancels the debt discharged by the loan servicer. To officially notify the Department of Education that the borrower has passed away, you will need to fill out a Death Discharge.

Who is responsible for private student loans after death?

You can answer this question with a question:

Was there a cosigner on the loan?

It’s rare to see a federal student loan borrower need a cosigner. However, private loans often require a cosigner. A clear majority (90 percent) of all private student loans have a cosigner, according to a 2014 report from the Consumer Financial Protection Bureau, the most recent data available.

If the primary borrower of a private student loan dies, the cosigner may very well find themselves responsible for repayment.

This does not apply to all cosigners. Not all private student loan lenders have the same policies regarding a borrower’s death. The outcome of this scenario may vary depending on the lender and the details of the loan.

If you’re a cosigner on a private student loan when someone passes away, make sure to read the lending agreement carefully to determine what happens if the primary borrower dies. If you’re still in doubt, call the lender to ask.

Who is responsible for Parent PLUS student loans after death?

Not all debts passed after death involve being married. Here is a debt that may be passed from a child to a parent — but in a way that you may not expect. The same rules as other student loans apply, but these loans are different than your typical direct federal loans.

Graduate and professional students are eligible to take out PLUS loans. The acronym PLUS stands for Parents of Undergraduate Student Loans.

So, parents take out these loans for their undergraduate students — without a cap on how much they can borrow — but an undergraduate student is not eligible to borrow this type of loan without one of their parents involved. When the child of a PLUS loan dies, that PLUS loan is canceled through a Death Discharge application.

If it’s the other way around and the parent passes away, the child (student) can put that loan to rest with a Death Discharge application. The student may die while having an outstanding PLUS parent loan. In that case, the debt dies with them, and the parents are not responsible for the debt.

If two parents cosign on the loan and one of the parents dies, the surviving parent will take responsibility for the loan repayments. Yes, the debt dies with the student; however, the borrower’s parents may find themselves with tax debt after the loan is discharged by the federal government.

You may be wondering how does that work?

The IRS may find that Parent PLUS loan to be an additional source of income. In that case, it can send the parent what is called a 1099-C or a cancellation of debt form. If this happens, the IRS considers the loan as an increase in your income. You are responsible for paying the taxes on the loan amount unless you qualify for an exemption.

What happens to your medical debt when you die?

Medical debt doesn’t just vanish after death for some people. There have been cases where family members have inherited the medical debt of relatives. It’s very uncommon, though. Depending on what state you live in, you may never have to worry about paying the medical debt of a deceased family member.

A very old law called filial responsibility is occasionally enforced in some states. Filial responsibility refers to laws that require adult children to repay medical bills that their parent or parent’s estate can’t afford.

Most states don’t impose these laws. However, there have been cases where hospitals and nursing homes have sued adult children to repay what they’re owed.

If your parents were in a nursing home or received long-term care up until their death and were unable to pay for the costs — you may end up stuck with a bill. Again, this is rare to happen.

This depends on your state and unique situation. Remember, this article is simply an informative guide and not legal advice.