As of 2024, about 22 percent of consumers in the U.S. with a credit file have a third-party collection tradeline furnished to their credit report. Unfortunately, not all of these third-party collectors are reputable. According to the Federal Trade Commission (FTC), harassing consumers to collect a debt is illegal, as it violates the Fair Debt Collection Practices Act. Since 2010, the FTC “secured permanent bans against 201 companies and individuals who engaged in serious and repeated violations of law, barring them from ever working in the debt collection industry again.”

To prevent abuse of power by debt collection agencies and individuals, the Fair Debt Collections Practices Act (FDCPA) was passed in 1977 and a report is published on it every year. All of the stats here are from 2024, the year of the most recent report.

So, how did things turn out for consumers facing collections in 2024?

Here are the stats…

General debt collection statistics

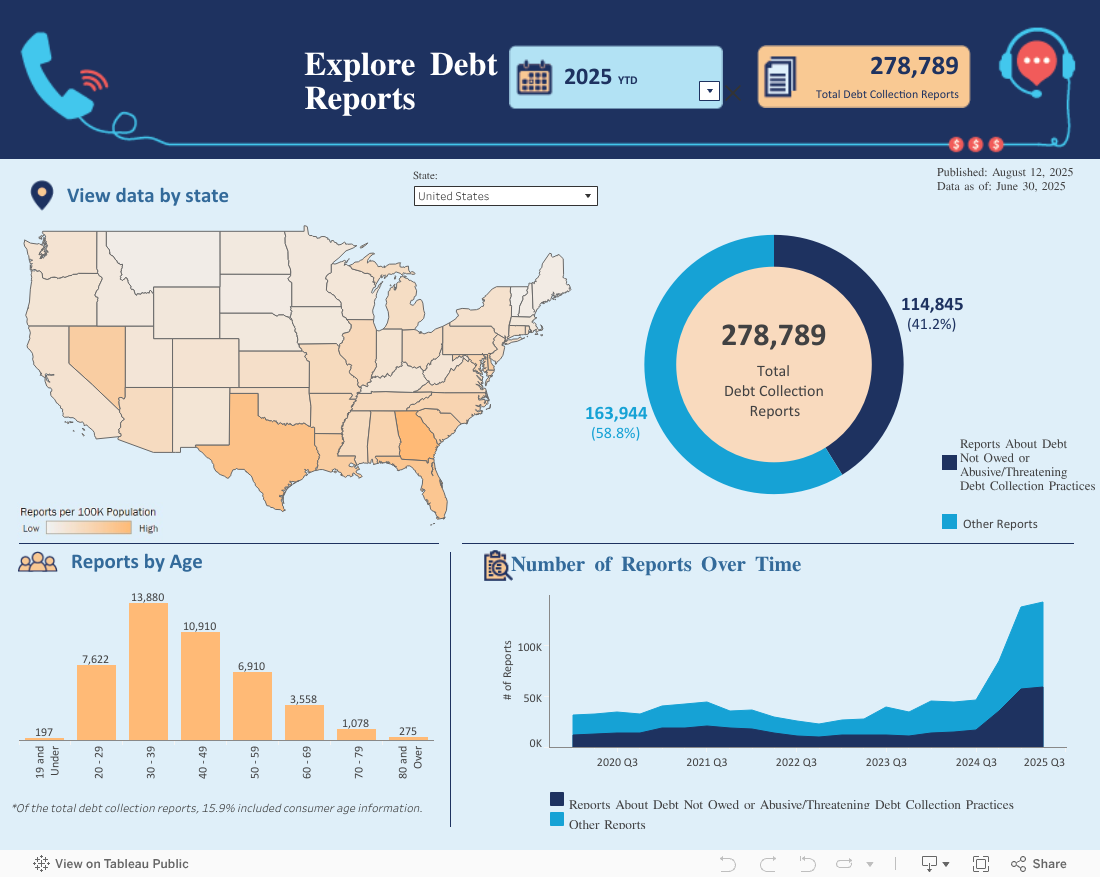

Number of complaints consumers filed against debt collectors in 2024 – 147,762

Total number of complaints received by the CFPB in 2024 – 2,646,567

- Credit reporting or other personal consumer reports: 2,297,591

- Debt collection: 147,762

- Credit card: 72,480

- Checking or savings account: 49,873

- Mortgage: 20,296

Method used to submit complaints…

- Web: 2,608,952

- Phone: 19,397

- Referral: 10,619

- Postal mail: 7,599

Top 5 issues consumers identified:

- Incorrect information on credit report: 1,153,362

- Improper use of credit report: 688,047

- Problem with existing investigation: 455,322

- Attempt to collect debt not owed: 66,796

- Written notification about debt: 46,398

Company responses to consumer complaints

- Closed with non-monetary relief – 1,147,169

- Closed with explanation – 1,060,224

- Company reviewing – 416,437

- Closed with monetary relief – 20,940

- The company did not provide a timely response – 1,785

Took or threatened to take negative or legal action (2023) – 10%

Of that 10%…

- 50% reported that collectors made threats or suggestions that their credit histories would be damaged.

- 17% reported that collectors made threats to sue for an old debt.

- 3% reported that collectors threatened to arrest or jail consumers who didn’t pay.

- 5% reported that collectors said they would try to collect exempt funds (i.e. child support or unemployment benefits).

- <1% reported that collectors threatened deportation or turning them in to immigration.

False statements or representations (2023) – 8%

Of that 8%…

- 77% said collectors tried to collect the wrong amount.

- 11% reported that collectors impersonated a government official or law enforcement official.

- 10% said collectors insinuated that they were committing a crime by not paying their debt.

- 2% said collectors told them they shouldn’t respond to a lawsuit.

Communication tactics (2023) – 7%

Of that 7%…

- 54% complained of frequent or repeated calls.

- 30% said they continued to receive communications after requests to stop

- 12% reported abusive language.

- 5% reported calls outside of the restricted calling hours between 8 AM and 9 PM.

Threatened to contact someone or share information improperly (2023) – 2%

Of that 2%…

- 61% complained that the collector talked to a third party about their debt.

- 12% said the collectors contacted an employer.

- 25% reported that collectors contacted the consumer after they asked them not to.

- 2% complained that the collectors contacted them directly instead of going through their attorney.

Struggling with unlawful or abusive collections?

As people struggle through As people struggle through the economic downturn caused by COVID-19, collections are on the rise. The CFPB has five action letter templates to help you correspond with collectors, as well as two new no-action letter templates. If you are facing abuse or threats, fight back today! Call Debt.com or complete the form to request help to end collector harassment now!